- Travel is back, with Canadian flight and hotel spending already above pre-pandemic levels.

- Hard hit by the pandemic, the industry is in for a post-crisis boost as high income Canadians channel hefty savings toward vacations.

- Demand is strong enough to power through inflationary pressures, even as they eat into household incomes.

- Current weaknesses, including business travel and COVID restrictions in parts of Asia, are set to be future sources of growth.

- The bottom line: the biggest concern for Canada’s travel businesses may well be supply: amid a historic labour crunch, the sector is still down 177,000 workers.

Canada’s travel industry is making a comeback

Hotels are open, restaurants are humming and after two years of pandemic staycationing, Canadians are travelling again. Fuelling that renewed wanderlust are higher household incomes, a much larger than normal savings trove, pent-up travel demand and fewer pandemic travel restrictions and health concerns.

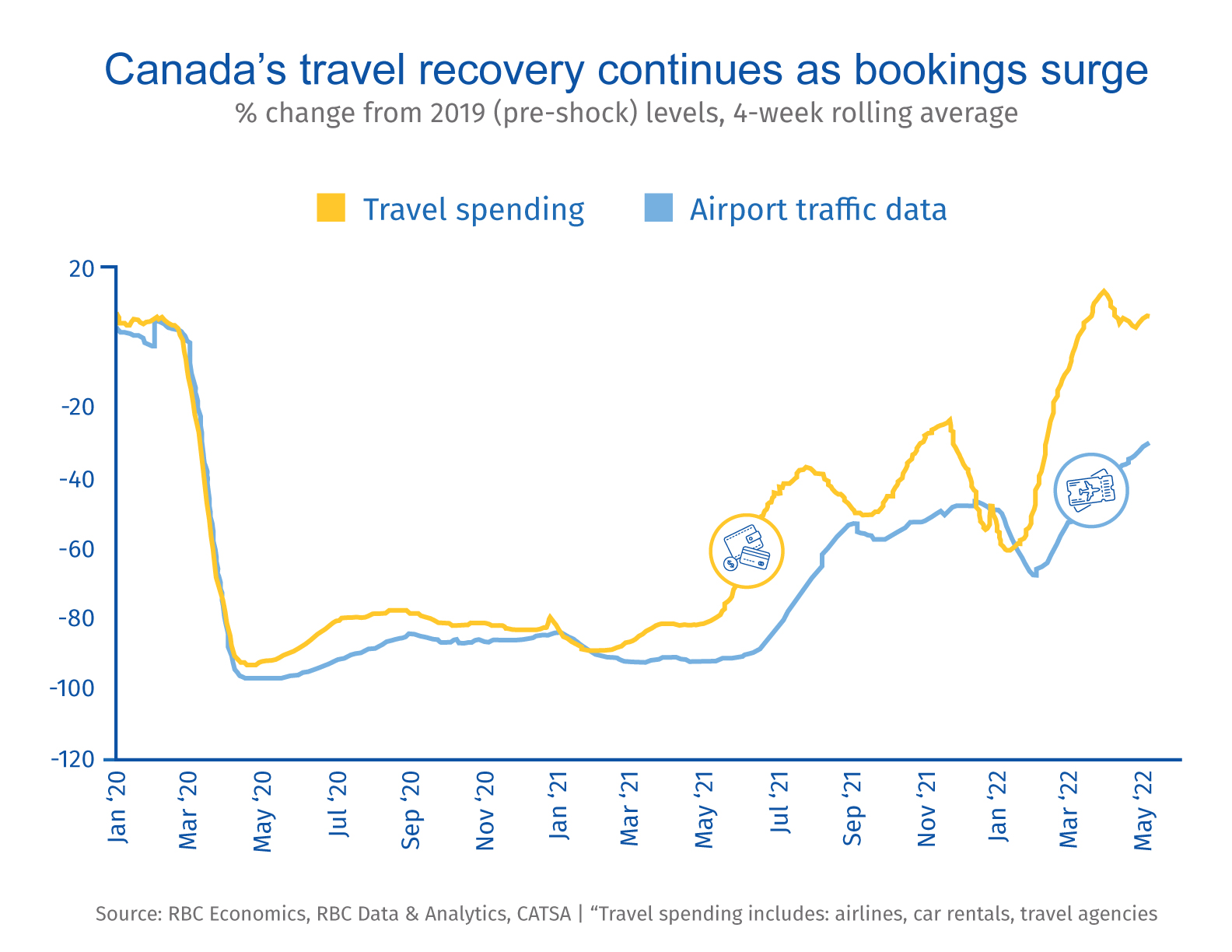

Passenger traffic at Canadian airports is still running 30% below pre-pandemic (2019) levels as of May. But our own tracking of debit and credit card transactions points to a surge in trip bookings, with purchases of flights and hotels (which often predate actual travel activity) booming back above pre-pandemic levels by mid-March.

Recovery firing through rising inflation and interest rates

Even as Canadians pack their bags and the economic impact of the pandemic eases, inflation is also on the rise. Central banks both in Canada and abroad are now hiking interest rates in an effort to cool demand and cap price growth. That’s eroding household purchasing power, but spending on leisure and travel is expected to push through it, at least in the near-term.

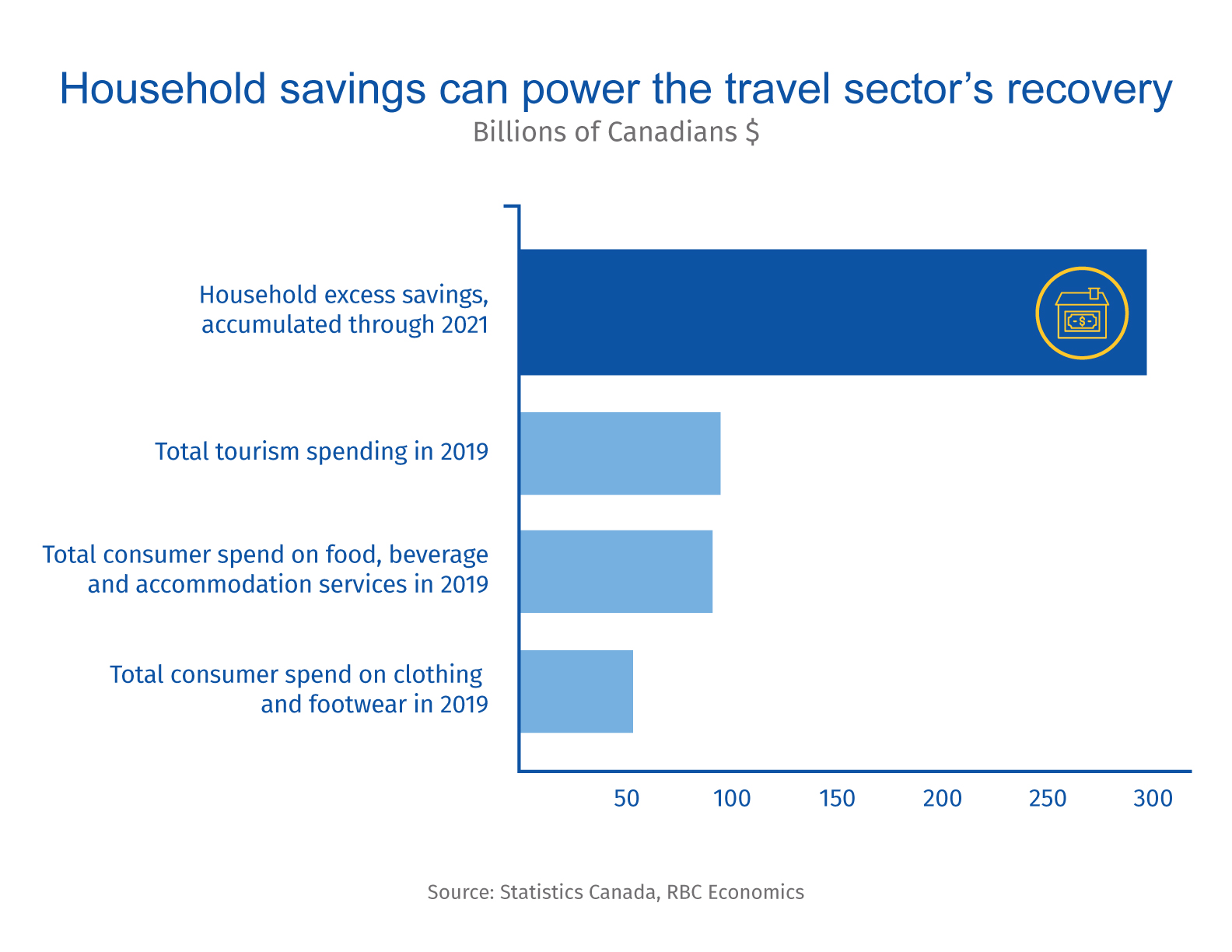

Canadians have the savings muscle to do it. Households accumulated a massive $300 billion savings stockpile during the pandemic, as health concerns and pandemic lockdowns restricted spending on leisure and hospitality services. Put in context, that’s three times what Canadians spent annually on tourism prior to the pandemic. And those savings have been disproportionately concentrated among higher income households that typically spend more on discretionary purchases, including travel. In pre-pandemic years, households from the top one-fifth income quintile accounted for over a third of total spending on hospitality services. By contrast, lower-income households, will feel the pinch of higher interest rates and inflation costs relatively quickly.

Worker shortage might cap growth, pushing prices higher

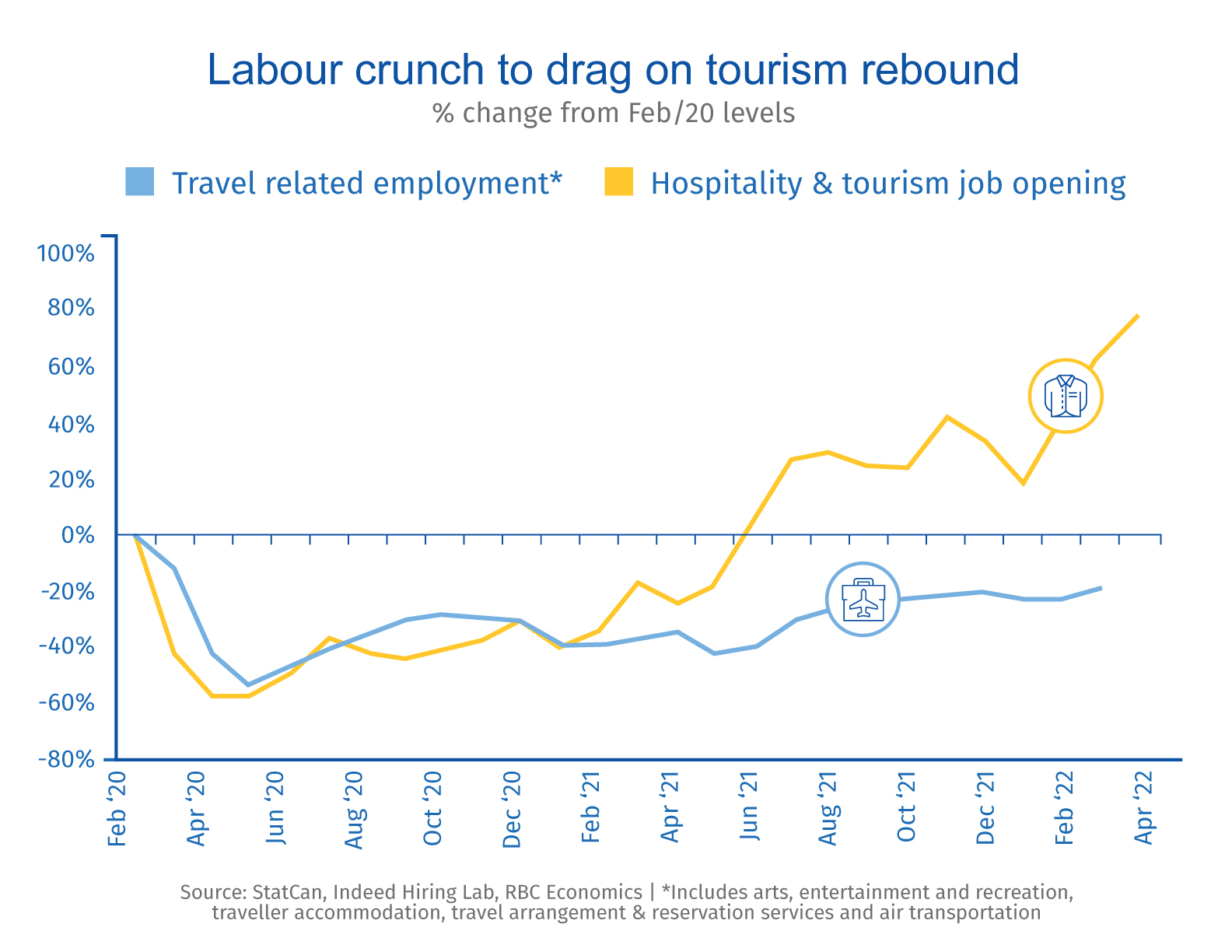

With travel demand booming, a more pressing question is whether supply will be able to keep up. Labour shortages are acute across sectors. That includes in travel-related industries where employment was still 177,000 short of pre-pandemic levels as of March. Businesses are trying to recoup those losses. In April, there were 80% more hospitality and tourism job postings than there were prior to the crisis in Canada. And with the unemployment rate at its lowest level (5.2%) on record since at least 1976, there simply is not a large pool of unemployed workers to hire from anymore. A sizeable share of workers in ‘higher-contact’ industries that were the most restricted during pandemic lockdowns have switched to other lower-contact (and often higher-paid) industries.

Meantime, a shortage of supply, and rising input, transport and labour costs are all pushing prices higher. In late 2021, pandemic-related disruptions to vehicle supply sent car rental prices surging as much as 60% above the prior year. Strong demand for workers will also accelerate wage growth. The impact of these factors have yet to surface in Canadian labour market data. But in the United States, wages in the leisure and hospitality sector have surged 11% over the last year. Prices for travel services have yet to recover fully, but have been growing at a faster rate recently—led by a recovery in airfares.

Some corners of travel will stay weak a little longer

International travel has been slower to rebound—and there will be limits to the recovery as long as the pandemic is still significantly disrupting activity abroad, particularly in parts of Asia where strict entry and quarantine requirements remain. Air travel from Asia in April was at just 32% relative to 2019, much lower than 59% from North America and 66% from Europe.

Business travel is another spot where the recovery could take longer. Prior to the pandemic, around 10% of trips made by Canadian residents were business related. Some of these trips may never come back, with the pandemic making the use of virtual meetings and events far more acceptable. International trips made for businesses purposes in Q4 2021 were just over half of levels in the same quarter in 2019.

That is not to say these areas of travel will stay weak forever. With the spread of COVID-19 and related health concerns both easing further, more countries will open up, allowing travelers with ample spending power to enter and deploy their savings.

Claire Fan is an economist at RBC. She focuses on macroeconomic trends and is responsible for projecting key indicators on GDP, labour markets as well as inflation for both Canada and the US.

Naomi Powell is responsible for editing and writing pieces for RBC Economics and Thought Leadership. Prior to joining RBC, she worked as a business journalist in Canada and Europe, most recently reporting on international trade and economics for the Financial Post.

Claire Fan is an economist at RBC. She focuses on macroeconomic analysis and is responsible for projecting key indicators including GDP, employment and inflation for Canada and the US.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.