Housing Trends and Affordability

Highlights:

- It was becoming less affordable to own a home when COVID-19 hit: RBC’s national aggregate affordability measure deteriorated (albeit just slightly) for a second-straight time in the first quarter of 2020.

- Rising housing costs in Ontario were the main culprit: Rapidly growing demand and tight supply cranked up the heat in markets across the province.

- COVID-19 pummeled housing activity from coast to coast: Home resales plummeted in March and April but so did supply. Both demand and supply partially recovered in May as the economy began to reopen.

- Market’s road to recovery will be long and bumpy: High unemployment and slower in-migration will restrain buyers’ return to the market. So could affordability issues in Vancouver, Toronto and Victoria.

- There’s scope for housing affordability to improve: We expect moderately lower home prices and exceptionally low interest rates to reduce home ownership costs in the period ahead. The risk of falling household income once government support programs expire could partly offset gains in affordability, however.

The share of income a household would need to cover ownership costs (in %)

Hot housing market hurt affordability before COVID-19 struck

The cost of owning a home took a slightly larger share of a household’s income in Canada in the first quarter of 2020—just as the global pandemic spread to our country. That share for a composite of all housing types (RBC’s aggregate affordability measure) inched 0.2 percentage points higher to 50.5%. This was the second-straight increase, marking a turnaround in property values in British Columbia and parts of Ontario. Downturns in these markets earlier led to a string of modest declines in RBC’s national affordability measure from mid-2018 to mid-2019. By the late stages of 2019, however, buyers and sellers had fully adjusted to policy changes made in 2017 and 2018 (including the introduction of a more stringent mortgage stress test). Demand-supply conditions had tightened again. So much so that fears of overheating resurfaced in Ontario this winter.

Affordability improved outside Ontario

Home prices in Ottawa, the Greater Toronto Area and other southern Ontario markets rose at some of the faster rates in the country in the first quarter of 2020. A modest drop in mortgage rates and solid household income gains attenuated the impact on potential homebuyers though it still became less affordable for them to own a home. In fact, Ontario was the only province where affordability deteriorated last quarter. RBC’s aggregate affordability measure rose in both Toronto and Ottawa. Lower mortgage rates and rising income more than offset price appreciation in British Columbia, Quebec and most of Atlantic Canada, or amplified the affordability-boosting effect of declining prices in the Prairies. St. John’s, Saint John, Quebec City and Regina recorded the most significant improvement in RBC’s measure last quarter. Vancouver, Toronto and Victoria continue to be Canada’s least affordable housing markets.

Long and bumpy recovery may lead to improvement in affordability

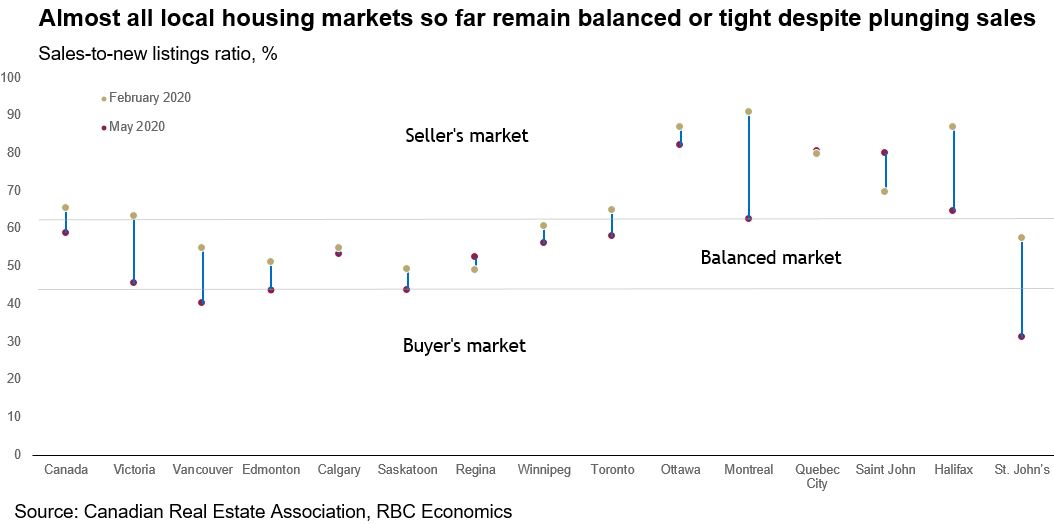

Price trends generally held up since governments declared states of health emergencies mid-March despite home resale activity plummeting 40% to 80%. That’s because supply fell in tandem. Demand-supply conditions have been quite resilient in most local markets so far. We expect conditions to loosen more in the coming months as economic hardship causes potential buyers (especially first-time buyers) to delay their purchasing plans, and financially-strained owners (including investors) sell their property once support programs run out. We believe the scale will tip in favour of buyers in many markets across Canada and (benchmark) prices will fall modestly, possibly as early as this summer. This, along with historically low interest rates, will reduce home ownership costs. The degree to which it translates into an improvement in housing affordability will depend on households’ ability to maintain their income. While the scope for such is limited near-term, we see the outlook brightening somewhat later this year as the economic recovery further progresses.

Market dynamics to keep an eye on

April was the low point for home resales virtually everywhere in Canada. Activity picked up in May as provincial economies began to reopen, and buyers and sellers became more comfortable transacting under physical distancing rules. We see these factors driving resales further up over the next few months. Then, we expect the market recovery to hit increasing resistance from high unemployment and lower immigration. Any signs of weakening prices could also shake confidence in the market, sending some buyers and sellers back to the sidelines. The path ahead will vary significantly by local market. Oil-producing regions are poised to experience a relatively slower recovery in both their economy and housing market. Growing adoption of work-from-home arrangements could shift some demand from expensive urban markets to more affordable smaller markets. This could potentially be a bigger issue for Vancouver, Toronto and the core of other large urban areas.

See Housing Affordability Measures

Robert Hogue is responsible for providing analysis and forecasts on the Canadian housing market and provincial economies. Robert holds a Master’s degree in economics from Queen’s University and a Bachelor’s degree from Université de Montréal. He joined RBC in 2008.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.