Canada’s housing market may be entering the latter stages of its cyclical downturn. The pace of decline is now slowing—there was even a tiny monthly increase in home resales nationwide in October—marking a notable shift from the deep fall in activity that took place over the spring and summer. Property values are still clearly coming down at this stage but last month’s drop was the smallest since May. While we continue to think an inflection point is some ways off, it does suggest most of the price correction is likely behind us—at least for Canada as a whole. Our view is that rising interest rates and the loss of affordability will keep market activity quiet into early-2023 and prices will bottom around spring.

First resales increase in eight months

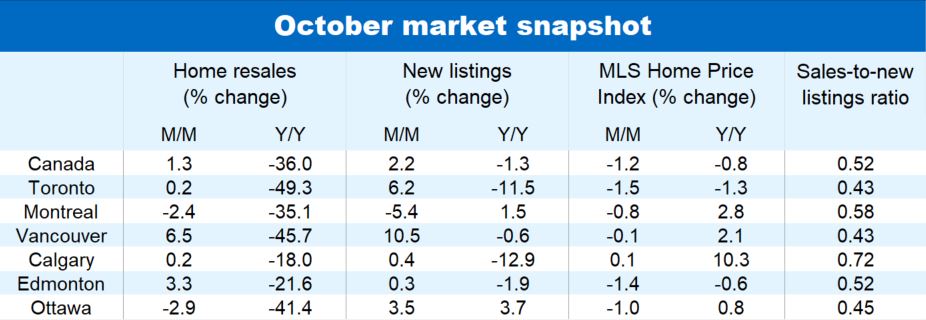

Home resales rose a slight 1.3% m/m in October across Canada to 424,600 units (seasonally adjusted and annualized). This potentially signals market activity is nearing a bottom after sliding 36% over the previous seven months. Among the small majority of local markets recording a monthly increase were Victoria (+19.7%), Vancouver (+6.5%), Edmonton (+3.3%), Saskatoon (+6.3%), Winnipeg (+2.2%), Hamilton (+1.7%), Saint John (+2.7%) and Halifax (+9.2%). Sales in Toronto and Calgary were essentially flat in the month (edging up just 0.2% in both cases), and fell further in Ottawa (-2.9%), Montreal (-2.4%) and Quebec City (-1.6%). The number of existing homes changing hands remained below—and often far below—year ago levels in virtually every market.

Price decline streak still going… but a little less strong

The fall in home prices has yet to be broken. The aggregate MLS Home Price Index for Canada slipped for an eighth straight month in October (down 1.2% from September). It slipped below its year-ago level (-0.8%) for the first time in three years and it’s now down 10% since the February peak.

While the erosion of property values is widespread across the country, the magnitude varies considerably. Properties in Ontario and British Columbia have seen the larger losses (after seeing some of the larger gains earlier in the pandemic). Cambridge (-22%), London (-18%), Brantford (-18%), Kitchener-Waterloo (-17%), Kawartha Lakes (-17%) and Hamilton-Burlington (-17%) have recorded the steepest MLS HPI drop since their cyclical peak earlier this year in Ontario. Chilliwack (-18%) and the Fraser Valley (-12%) have led the decline in British Columbia.

Affordability issues weigh big on Toronto and Vancouver prices

The correction shaved another 1.5% off the Toronto-area MLS HPI last month. It’s now down more than 11% since the February peak (on a seasonally-adjusted basis). The downturn has so far been comparatively less severe in Vancouver. Its MLS HPI has fallen 5.3% since cresting in March. And the monthly rate of decline moderated significantly in October to just -0.9%. We doubt this will mark a turning point. We expect extremely poor affordability conditions will maintain intense downward pressure on property values in the area. The same goes for Toronto where were see prices continuing to fall in the near term.

Calgary: the exception to the rule

There are very few markets bucking the general weakening trend. Calgary is one of them. While activity is down from sky-high levels at the start of this year, it’s still far above pre-pandemic levels. And prices are holding up. The area’s MLS HPI has essentially been stationary since April. We expect this to continue as demand-supply conditions are among the tightest in Canada.

Market unlikely to heat up anytime soon

The market downturn may be in a late stage but it doesn’t mean things are about to heat up again. We expect high— and still-rising—interest rates will continue to challenge buyers for some time. This will keep activity quiet for a while longer even if it stabilizes near current levels. We think benchmark prices will keep trending lower until spring.

See PDF with complete charts

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.