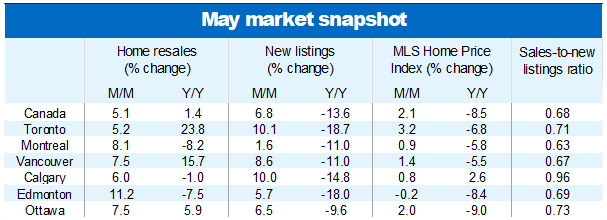

Canada’s housing market is picking up steam. Both home resales and prices continued to rise at rapid clips in May. And odds are they will climb further in June with more properties now becoming available for sale. A solid 6.8% m/m increase in new listings last month helped unlock some of the pent-up demand that built during the year-long correction.

The recovery to date is stronger than we expected. Our view was activity would rebound slowly at first due to ongoing affordability issues that would hold back many buyers. The Bank of Canada merely pausing its interest hike campaign earlier this year appears to have rekindle demand in a material way this spring. Still, we question the sustainability of that strength beyond the next month or so. The Bank of Canada’s (mildly) surprising rate hike in June and the prospects for further monetary policy tightening are likely to temper the pace.

Home resales rapidly normalizing toward pre-pandemic levels

The increase in homes for sale set the stage for a solid 5.1% m/m jump in purchase transactions nationwide in May. This came on the heels of an even sharper 11.3% spike in April, which together significantly narrowed the gap with pre-pandemic levels. Home resales are now just 6% below their (vibrant) February 2020 level.

Broad recovery

The upturn over the last two months has been a central theme from coast to coast. Transactions increased significantly in all provinces, led by British Columbia (up 23%) and Ontario (up 22%). Gains were especially strong in the Vancouver (35%) and Toronto (32%) areas between March and May— albeit from historically depressed levels in both cases. For now, activity is still running below pre-pandemic levels in the majority of markets except in Alberta and Saskatchewan where it never dipped below those levels during the correction.

Prices go up for the second consecutive month

After falling more than 15% from its February 2022 peak, the national composite MLS Home Price Index rose 4.1% in the last two months, including a 2.1% m/m gain in May. This is on-par with the average monthly rate of increase during the most recent market boom. Prices appreciated sharply last month in several Ontario markets, including Cambridge (up 4.9% m/m), Northumberland Hills (up 4.7%), Sudbury (up 4.5%), Kitchener-Waterloo (up 3.6%), Kawartha Lakes (up 3.2%) and Greater Toronto (up 3.1%). The Fraser Valley (with its MLS HPI rising 2.4% m/m) led British Columbia, Winnipeg (up 0.9%) led the Prairie Provinces, and Halifax (up 1.8%) led the provinces east of Ontario.

Prices generally remain below year-ago levels but possibly not for long in parts of Western Canada, Quebec and the Atlantic Provinces. Current upward momentum and declining trends last year are poised to boost annual rates into positive territory in the period ahead. Calgary is among the few markets where prices never dipped on a year-over-year basis during the correction.

Sellers hold significant pricing power

Spurts of new listings across the country eased demand-supply conditions in the majority of markets last month. But not enough to tip the scale in favour of buyers. In fact, sellers continue to hold the stronger hand at this point, which is why prices have been appreciating lately.

We expect conditions to ease some more in the period ahead, however, bringing markets closer to balance. Our forecast for another 25 basis-point rise in the Bank of Canada’s policy rate should cool demand by a few degrees—at least for a time. We see more balanced conditions moderating the pace of price increases, not triggering outright declines.

Current pace is likely unsustainable

Our view is the current strength in the market is unlikely to be sustained through the remainder of this year. We continue to believe that the more probable scenario is a gradual recovery in both resales and prices until the Bank of Canada starts cutting rates next year. That said, we’ve been surprised by the market’s vigour to date and we could certainly continue to be going forward.

See PDF with complete charts

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.