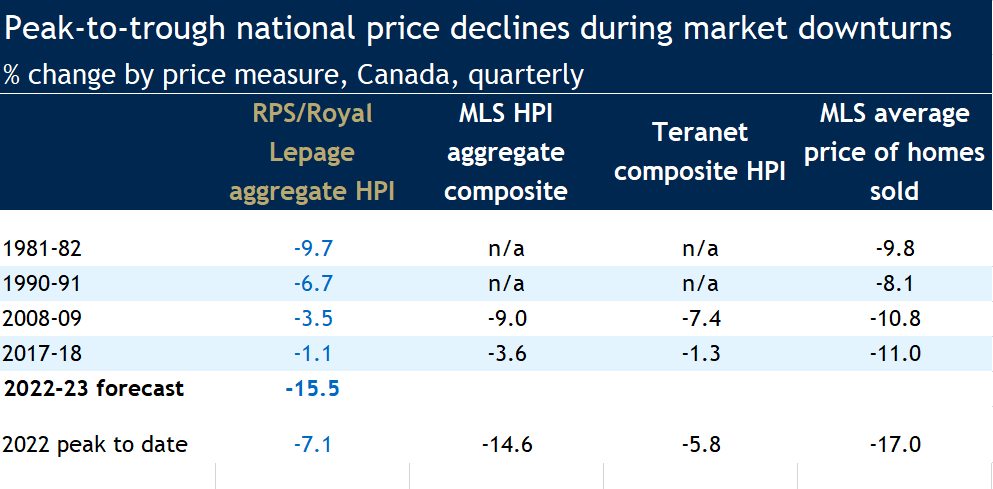

The Canadian housing market correction has yet to run its course but it’s gradually letting up. We think activity will hit bottom sometime this spring. Prices will level out a few months later—provided the Bank of Canada is done raising interest rates. All told, our forecast calls for a 15% peak-to-trough decline in the national RPS Home Price Index. Roughly half of that is still to come.

What happens next will disappoint housing bulls. We see the recovery phase starting slowly later this year as affordability issues and a weaker economy continue to hold back buyers. The pace should progressively pick up in 2024 once the economy clears its soft patch, inflation returns to target and the Bank of Canada reverses part of the massive rate increases it’s imposed since March 2020.

Booming immigration will fuel demand through the medium term (and possibly beyond), raising the odds of deep supply shortages in the future if homebuilding fails to pick up materially.

Activity can’t get much quieter

A precipitous slide in home resales has ended a two year market frenzy that kicked off in March 2020. But this slowdown has significantly moderated since the fall. The primary reason: activity is now deeply depressed in most markets, and unless the economy craters (not our base case), there’s little downside left. Accounting for the growth in housing stock, nationwide resales are the quietest they’ve been since the 2008-2009 global financial crisis (excluding the lockdown period in the spring of 2020). We believe a bottom will form in the coming months. Some markets might be ahead of the pack (e.g. in Ontario and possibly Atlantic Canada), while others (e.g. in the Prairies and Quebec) might lag somewhat.

Bank of Canada may be done hiking rates, but it’s not about to cut

Another reason: the Bank of Canada’s rate hiking cycle is now likely on hold. We think January’s 25 basis-point hike will be the final strike in a historic campaign that drove the policy rate up by a staggering 425 basis points, taking it to 4.5% in less than a year. Market sentiment should get a boost when participants come to that conclusion. Any downward drift in longer-term bond yields—which is RBC’s call over the next year—is also likely to be viewed as a positive sign of a turnaround. But these factors will help stabilize the market, not prop it up. We see the interest rate environment remaining restrictive for a while and the Bank of Canada abstaining from cutting rates until 2024.

Affordability issues to ease, but only gradually

This means the sharp deterioration in housing affordability since 2021 won’t unwind quickly. Buyers will continue to face steep challenges, especially in B.C., Ontario and other expensive markets where ownership costs have ballooned during the pandemic. Lingering affordability issues will stand in the way of a quick market rebound and a material easing in buyers’ budget constraints.

Prices have further to drop in the near term

We expect home prices to continue declining in the coming months as a result. The national RPS HPI is likely to fall another 8% by the third quarter from fourth quarter levels—with markets in B.C. and Ontario still bearing the biggest downside risk. Our peak-to-trough price forecasts range from -19% in Ontario and -16% in B.C. to -6% in Alberta and -5% in Newfoundland and Labrador.

Other price measures (e.g. MLS HPI and MLS average sales price) have already exceeded our national peak-to-trough forecast of -15%. That’s largely because these measures are more volatile than the RPS HPI. They soared higher during the dramatic run-up earlier in the pandemic and responded more quickly to the downturn—as has typically been the case in prior cycles.

Solid market fundamentals despite it all

The dramatic swing in the market since March 2022 is a cyclical event marking the transition out of highly unusual circumstances—a global pandemic and exceptionally low interest rates. Structurally the market is sound. Inventories are still historically low (albeit rising modestly) and there are no signs of overbuilding virtually anywhere in the country. Canada’s population has grown the most in generations over the past year, and booming immigration will keep that going over the medium term. We believe solid fundamentals will come to the fore in 2024 once the market has adjusted to higher interest rates.

Homebuilding the key to longer-term balance

Could things heat up to an uncomfortable degree again in the future? We certainly wouldn’t rule it out. It’ll all come down to the supply response. And on that front, the recent track record for construction has been underwhelming. While homebuilding has picked up in Canada over the past three years—housing completions rose from less than 190,000 units in 2019 to roughly 220,000 units in 2021 and 2022—it was nowhere near enough to meet supercharged demand. We estimate that our housing stock must expand by at least 270,000 units per year by 2025 just to accommodate the growth in households, let alone address the housing affordability crisis in many Canadian cities. Needless to say, homebuilding needs to ramp up considerably from this point on. It’s unclear, though, whether the construction industry has the capacity to do so in the face of significant labour shortages.

Read the full pdf report including additional tables

Read full report

Robert Hogue is responsible for providing analysis and forecasts on the Canadian housing market and provincial economies. Robert holds a Master’s degree in economics from Queen’s University and a Bachelor’s degree from Université de Montréal. He joined RBC in 2008.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.