Canada’s housing market has calmed down considerably this summer, taking some of the heat off property values across many parts of the country. Home prices are still rising—the composite MLS Home Price Index in August was up a whopping 21.3% from a year ago and 0.9% from July. It’s just that the pace of increase isn’t as frenetic as it was earlier this year. The average 0.8% m/m rate of increase over the past three months is less than a third the 2.6% rate recorded in the first quarter (and less than half the July 2020-March 2021 2.0% pace). We expect further moderation in the period ahead as affordability issues weigh more heavily on buyers, the reopening of spending avenues take some budget room away from housing and the latest tightening in the mortgage stress test proves a bigger constraint for some. But widespread price declines aren’t in the cards. Exceptionally tight demand-supply conditions in most markets will continue to provide solid protection against any major price corrections though we see prices flattening by early-2022.

(Slightly) more sellers came to market in August

After four consecutive monthly declines, new listings increased 1.2% from July across Canada. Vancouver (up 12.7% m/m), Kitchener-Waterloo (up 8.9%) and Montreal (up 3.7%) saw larger increases. While these gave buyers more options to pick from, they were drops in a bucket in markets starved for inventory. Supply still falls well short of demand, significantly constraining activity. Such constraint in fact grew last month in Ottawa, Calgary, Edmonton and Toronto where new listings fell further.

Cooling trend persists but home resales still strong

The transition toward more sustainable levels of activity continued in August though the rate of cooling eased off materially nationwide (to -0.5% m/m) from the previous four months (-7.9% on average). The slight increase in new listings no doubt contributed to slowing down the pace of decline. We expect supply availability to remain a central factor charting the path of home resales in the coming months. A further uptick in sellers would work to stabilize activity—or even potentially boost it slightly, given the strength in demand. Failing that, however, we’d expect the cooling trend to take resales down closer to their (historically strong) pre-pandemic levels. Either way, we see activity remaining solid in the near term.

Low supply, soaring prices taking a toll on smaller markets

Recent cooling trends have been especially pronounced in smaller markets. Home resales have fallen back to, or below, pre-pandemic levels in parts of BC (including Chilliwack, Kamloops and Kootenay) and Ontario (including Barrie, Brantford, Cambridge, Guelph, Hamilton, Kingston, Kitchener-Waterloo and southern Georgian Bay). For the most part, this reflects severe supply shortages the pandemic housing boom created in those areas. Demand-supply conditions remain super-tight despite lower activity levels. But soaring prices no doubt have also dented demand. Smaller markets’ affordability advantage over their larger counterparts has eroded, particularly compared to downtown condos which have appreciated much less in value during the pandemic. Big-city buyers’ interest in smaller markets is likely being put to the test.

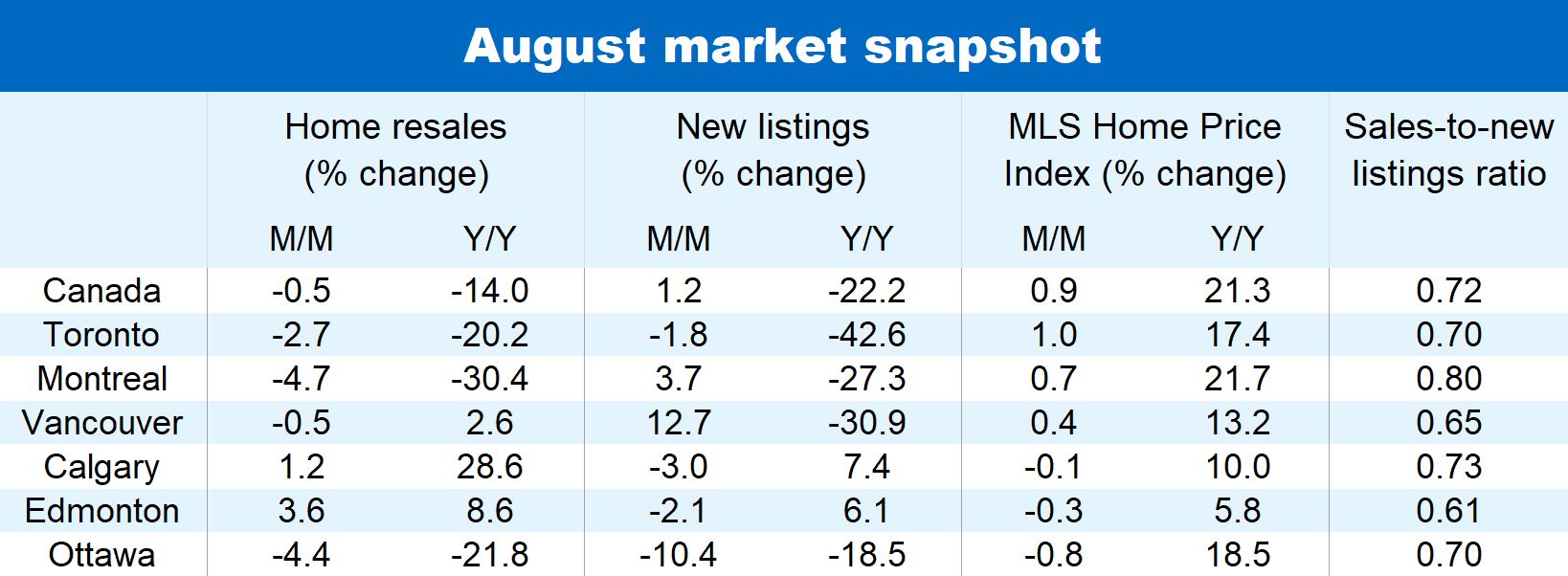

August Market Hightlights

- Price momentum slowed again: Canada’s composite MLS Home Price Index rose 0.9% m/m in August to $736,600. The index was up 21.3% from a year ago, down from 22.4% in July and a cycle high of 24.6% in June. The pace moderated materially in Ottawa (from 23.3% y/y in July to 18.5% in August) and Montreal (from 23.4% to 21.7%) to a lesser extent.

- Homes newly listed for sale inched higher for the first time in five months: New listings picked up 1.2% m/m nationwide, with a small majority of local markets recording an increase. Vancouver (up 12.7% m/m), Kitchener-Waterloo (up 8.9%), the Fraser Valley (up 5.5%) and Montreal (up 3.7%) led the way with the larger increases. Ottawa (-10.4%), Winnipeg (-6.5%), Calgary (-3.0%), Edmonton (-2.1%) and Toronto (-1.8%) recorded declines.

- Resales fell further but by less: Sales dropped just 0.5% from July in Canada—the slowest pace of decline of the current cooling phase. At 580,500 units (seasonally adjusted and annualized), resales remained strong historically and still far above the 533,200 level that prevailed just prior to the pandemic. Activity fell in a majority of markets, including Regina (-11.9% m/m), Winnipeg (-7.0%), Kitchener-Waterloo (-6.6%), Montreal (-4.7%), Toronto (-2.7%) and Vancouver (-0.5%). The Fraser Valley (up 9.9%), Edmonton (up 3.6%) and Calgary (up 1.2%) were among the few recording an increase.

- Sellers’ grip on the market slips a little but still very firm: Demand-supply conditions in Canada eased slightly in August.The national sales-to-new listings ratio fell to 0.72 from 0.74 in July—still consistent with very favourable conditions for sellers. This was generally the case across the country with only the degree of sellers’ advantage varying from market to market. More balanced conditions have recently emerged in some Prairie markets, including Regina, Saskatoon and Edmonton.

See PDF with complete charts

Robert Hogue is responsible for providing analysis and forecasts on the Canadian housing market and provincial economies. Robert holds a Master’s degree in economics from Queen’s University and a Bachelor’s degree from Université de Montréal. He joined RBC in 2008.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.