March brought a mixed bag of activity to Canada’s housing market. Resales continued to linger around February levels at the national level—still softer than activity that took place pre-pandemic.

As in recent months, activity was largely bogged down in Canada’s more expensive markets (including Toronto and Vancouver), where housing unaffordability is particularly acute. We suspect a standoff between (inflexible) sellers and (budget-constrained) buyers is developing. Widespread month-over-month drops in new listings may have be a restraining factor as well.

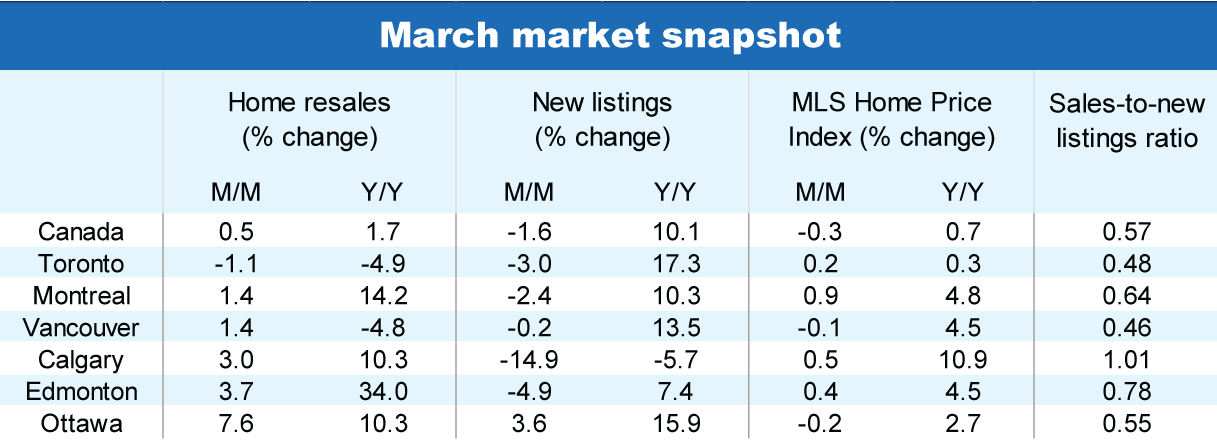

March sales essentially flat in Canada

Seasonally adjusted m/m sales were up just 0.5% nationwide, subdued mainly by slower activity in Ontario (-1.6% m/m)—including Toronto—Saskatchewan (-2.3%) and New Brunswick (-8.7%) while B.C. stayed the course (+0.7%). Alberta (+3.6%) and Quebec (+2.4%), on the other hand, saw a discernable pick-up in activity—including Edmonton and Montreal.

It’s worth noting seasonal factors have been larger than usual in recent months given the extra workday in February (from the leap year) and the Easter holiday landing in March this year (it was in April in 2023). We expect fewer seasonal distortions later this spring, which should give a truer reading of underlying market trends.

Buyers and sellers at a standstill

Supply-demand conditions remained generally balanced in Canada, though favouring sellers in some markets (e.g. Calgary). Some potential sellers may have held off listing their property in March in anticipation of stronger demand in the summer. There are growing expectations the Bank of Canada will cut interest rates mid-year.

Sellers looked especially cautious in B.C. and Ontario last month where price trends are still softening in many markets. Buyer enthusiasm, while generally recovering, is still lacking, and the sales-to-new listings ratio remains on a downtrend in these provinces.

Renewed market vigour in Quebec, on the other hand, brought supply-demand conditions to their tightest point since last summer. Most Alberta markets are extremely tight too, with the sales-to-new listings ratio in Calgary and Edmonton near all-time highs. We see greater price growth coming out of these markets in the months ahead.

Conditions are generally favourable to sellers in Atlantic and other Prairie provinces as well, setting the stage for modestly appreciating prices later this spring.

Prices levelling off

Canada’s MLS Home Price Index fell marginally by 0.3% m/m in March, following no change in February. Together they provide evidence Canada’s price correction has run largely its course. That said, local trends vary widely across the country.

A severe lack of affordability has kept prices down in many Ontario and B.C. markets—including Brantford, Cambridge, Ottawa, Fraser Valley, and Vancouver. The GTA, however, recorded its second consecutive monthly increase (+0.3%). Nova Scotia prices are also under downward pressure.

Other provinces are seeing prices continue to climb. Among the larger markets, sizable gains were recorded in Montreal (+0.9% m/m); Calgary (+0.5%) and Edmonton (+0.4%).

We expect prices to rise gradually in the coming months, and then accelerate progressively once the Bank of Canada’s rate cuts accumulate over the second half of this year and into 2025.

Slew of policy announcements to impact the market down the road

The policy response to Canada’s housing crisis has kicked into high gear in recent weeks. The federal government has announced a series of significant initiatives designed to tamp down housing demand growth, expand the housing supply (especially rentals) and make it easier for first-time homebuyers to become homeowners. Ontario also introduced legislation to speed up housing construction. We are encouraged to see policy action focusing on growing Canada’s housing stock, including the emphasis on rental apartments. Our report The Great Rebuild: Seven ways to fix Canada’s housing shortage warned that significant progress toward boosting supply is needed urgently to address the crisis. We believe the policy measures that were announced will bring relief over time. But they aren’t quick fixes.

See PDF with complete charts

Robert Hogue is an Assistant Chief Economist at RBC responsible for providing analysis and forecasts on the Canadian housing market and provincial economies. He joined RBC in 2008.

Rachel Battaglia is an economist at RBC. She is a member of the Macro and Regional Analysis Group, providing analysis for the provincial macroeconomic outlook. She holds a Bachelor’s degree in Economics (honours) from the University of Western Ontario and a Master of Science from the Amsterdam School of Economics.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.