Housing Trends and Affordability

Highlights:

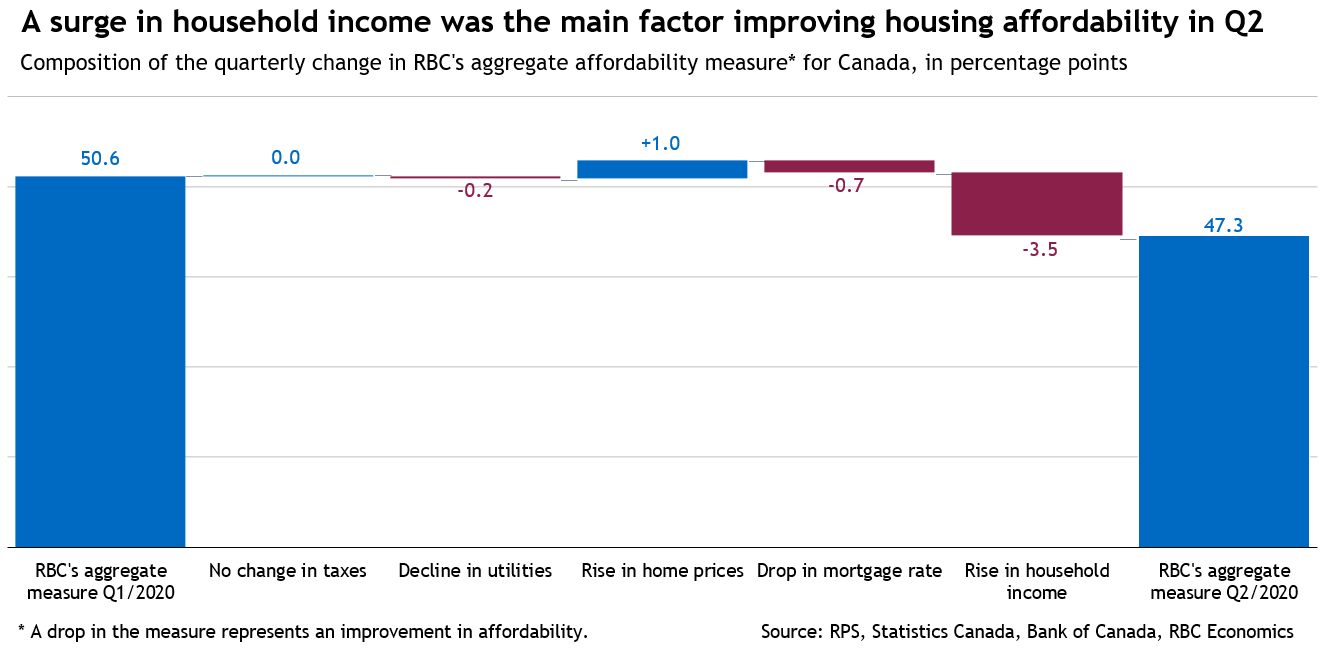

- Massive aid programs boosted housing affordability to a four-year best in the second quarter: RBC’s national aggregate measure dipped 3.3 percentage points to 47.3%—the most affordable level since mid-2016. Material improvements were recorded in all markets across the country.

- Affordability would have deteriorated slightly without COVID-19 income support: A surge in household income more than offset higher ownership costs. A drop in mortgage rates also helped.

- An average buyer could afford an average home in the majority of markets: This still wasn’t the case in Victoria, Vancouver and Toronto, however, where sky-high prices continue to pose a major hurdle.

- Second-quarter relief may prove fleeting: While the timing is uncertain, governments will eventually phase out income support programs. This will unwind last quarter’s income-related boost to affordability. The recent heating up in home prices could accelerate the process—though exceptionally low mortgage rates will be a moderating factor.

The share of income a household would need to cover ownership costs (in %)

Unprecedented income support took centre stage

Widespread lockdowns to contain the spread of COVID-19 delivered the biggest, most sudden shock in generations to Canada’s economy this spring. But they also prompted unprecedented government action to financially support households affected by the pandemic. The net result of it all has been a dramatic shift in home resale activity from spring to summer, and a (perhaps surprising) material improvement in housing affordability. Overall, Canadian households received more money ($56 billion) from government aid programs such as CERB and other transfers in the second quarter than they lost in wages and salaries due to the pandemic ($23 billion). On net, household disposable income spiked 11% in Canada. This substantially increased buyers’ purchasing power that forms the basis of RBC’s affordability measures. The income rise alone subtracted an outsized 3.5 percentage points from RBC’s aggregate measure for Canada last quarter (a decline represents an improvement in affordability). This was more than the total 3.3 percentage-point quarterly drop in the measure. Lower mortgage rates and a slight decline in utilities further helped improve affordability though an increase in home prices provided a partial offset. At 47.3%, RBC’s aggregate affordability measure was at its best level in four years. This no doubt greased the wheels of pent-up demand that powered the rebound in market activity this summer. Yet the temporary nature of the income swing heavily distorted the picture. RBC’s measure would have deteriorated marginally last quarter had it not been for the surge in income. Moreover, the picture varied considerably among Canadians with workers in many service industries being hit particularly hard by social distancing restrictions.

It’s important to note mortgage payment deferrals did not feed into the RBC measure’s calculations. Our methodology assumes mortgage payments are paid in full each month.

It became more affordable to buy a home from coast to coast

The massive income boost was pervasive and drove substantial affordability improvements everywhere in Canada. Victoria, Vancouver and Toronto recorded the largest declines in RBC’s measure though decade-strong drops took place in virtually all markets we track. The measure fell below its long-run average in the majority of markets, which indicates better than normal affordability in large parts of the country. But significant issues persist in Canada’s largest cities. Owning a home in Vancouver, Toronto and Victoria continues to be a huge stretch for an average household despite significant improvement in the second quarter. The bar also remains high in Montreal and Ottawa. Affordability stress in these large markets is more much intense in the single-detached home category where prices are steepest. Condo apartments, on the other hand, are a generally more achievable option, especially for first-time buyers.

Second-quarter affordability boost is poised to be short-lived

We expect household income to gradually normalize as pandemic support programs are phased out, re-focused or re-calibrated. Everything else being equal, a return to pre-pandemic income levels would effectively roll back all of last quarter’s substantial gain in affordability. Whether this will take place over the next few quarters is uncertain though any move in that direction will erode affordability. So will rising home prices. Tight demand-supply conditions have led to an acceleration in property values in many markets—a trend we think will be generally sustained in the near term. Recent declines in mortgage rates will provide some offset, however. Buyers in Canada’s least affordable markets—Vancouver, Toronto and Victoria—are most vulnerable to any erosion of affordability given how stretched they already are. Buyers are more likely to take things in stride in most other markets.

Price trends set to diverge

The impact of COVID-19 on the housing market is complex, and we believe it will lead to diverging price trends among regions and housing categories. The pandemic is affecting demand and supply of various market segments quite differently. It is cooling demand for and boosting supply of rentals in large urban areas. This, in turn, is reducing investor interest in condos. The pandemic is also altering the housing needs of many current owners who look for more spacious properties in less crowded settings. This is simultaneously shifting demand from condo apartments to single-detached homes and other low-rise categories, and increasing the supply of smaller condos in core urban areas. Work-from-home arrangements and the lesser appeal of big-city living (with reduced cultural and socializing opportunities during these times of social distancing) are increasingly driving buyers further away from downtown locations into suburbs, exurbs and even cottage country. We believe this trend will sustain strong demand in smaller markets, putting intense pressure on their housing stock. The bottom line is we expect condo prices to weaken in larger markets next year, while we see prices for single-detached homes remaining generally resilient—albeit increasing at a slower pace.

Read the full Housing Trends and Affordability report for extensive market-by-market analysis.

Read full report

Robert Hogue is responsible for providing analysis and forecasts on the Canadian housing market and provincial economies. Robert holds a Master’s degree in economics from Queen’s University and a Bachelor’s degree from Université de Montréal. He joined RBC in 2008.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.