Food is again at the forefront

The world needs a new Green Revolution, and Canada can play a leading role. Indeed, we must.

By 2050, we must increase our food production by a quarter just to maintain our contribution as the world’s population swells. We need to grow more for humanity, with less impact on the planet. This can be Canada’s moonshot for 2030 and beyond, if we can harness the imagination and enterprise of Canadians in every sector and geography.

The coming age of disruption, in agriculture and food systems, compelled RBC, BCG Centre for Canada’s Future and Arrell Food Institute at the University of Guelph to take on this project, to help inform and inspire Canadians to see both the urgent need and growing opportunity that will come with more sustainable food systems.

The following report outlines how we can build those systems by:

- Using breakthrough technologies as well as some well-established practices,

- Attracting and training a new generation of farm and food innovators,

- Investing in farmers to develop new economic incentives that reward what they produce as well as what they preserve,

- And boldly declaring to the world that Canadian agriculture can help everyone move more quickly to a world that has solved the climate crisis.

How we grow, process and consume food is not the key cause of our climate crisis. It can be a key solution. And with the right investments, it can become a made-in-Canada, farmed-in-Canada solution for the world.

- John Stackhouse, Senior Vice President, RBC Economics and Thought Leadership

Keith Halliday, Director, BCG Centre for Canada’s Future

Evan Fraser, Director, Arrell Food Institute at the University of Guelph

Key findings

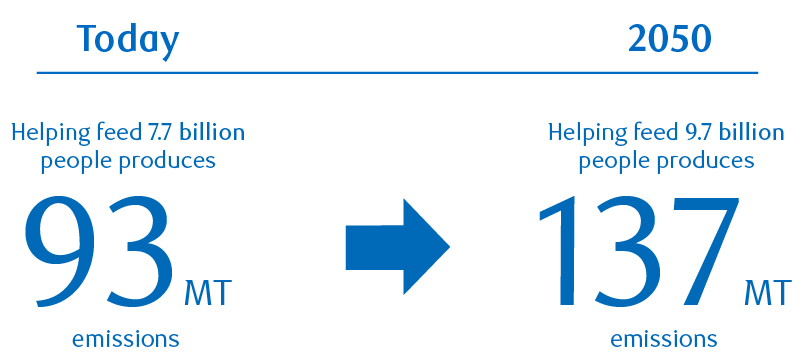

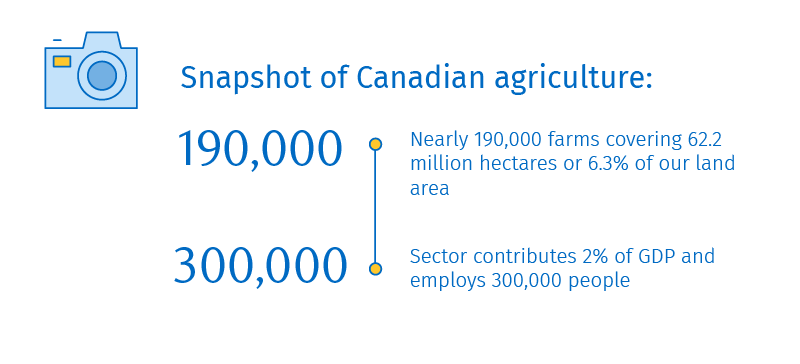

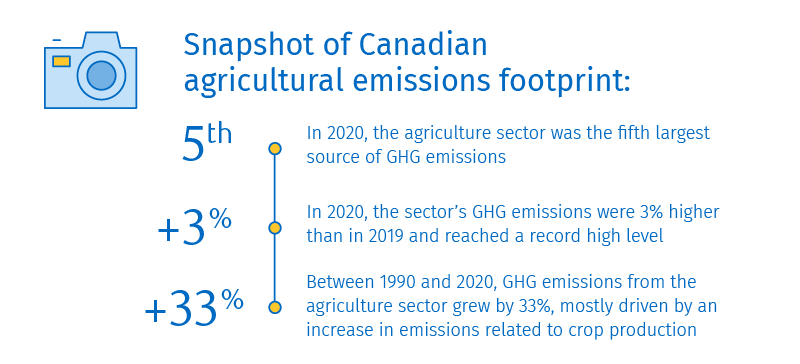

Canada’s agriculture and food systems produce 93 megatonnes or just over 10% of our national greenhouse gas emissions annually.1

If Canadian farmers maintain current practices and market share, these emissions could rise to 137 megatonnes as the world’s population increases 26% by 2050.2

Key technologies and approaches that can cut emissions include carbon capture, utilization and storage, feed additives, anaerobic digesters, and precision technology.

Nature-based solutions that sequester carbon will also be critical. Soil carbon has the potential to be one of our most powerful tools, raising the amount of carbon stored in soil to as much as 35MT.

By engaging these technological and management solutions, and mobilizing finance and policy to support farmers, Canada can cut up to 40% of potential 2050 emissions.

New models are needed to reward the adoption of these solutions, to execute them at scale and to reduce uncertainty and risk for farmers.

A Canadian standard for measuring the impact of emissions-cutting activities could provide a vital tool for both compensating farmers and empowering policymakers and financial institutions to support activities.

A national effort, tailored to regional contexts and focused on the key pillars of technology, finance, skills and public policy, will be essential to increasing our production while also cutting emissions.

Leading a low carbon farming revolution

Canada’s agricultural sector is at a turning point.

Global food demand is set to soar as the population rises to 9.7 billion in 2050—a 26% jump.3 At the same time, climate change is disrupting the supply chains and agricultural productivity of many major producers. And geopolitical upheaval from Russia’s invasion of Ukraine has destabilized the world’s food systems.

Rarely has feeding the world presented such a daunting challenge. Canada can lead the worldwide effort to confront it.

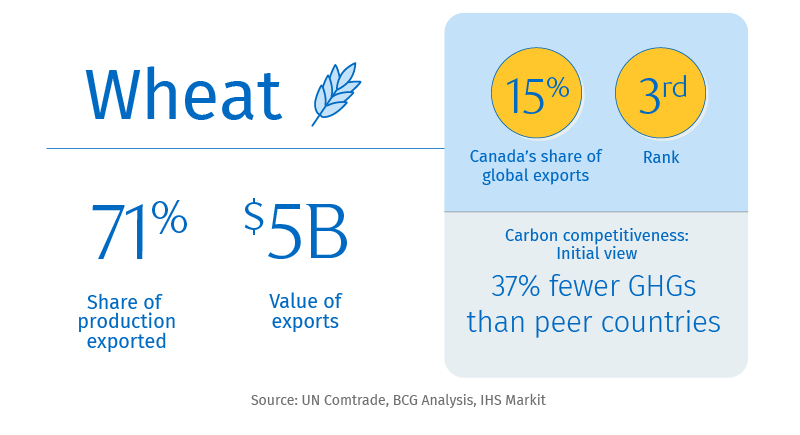

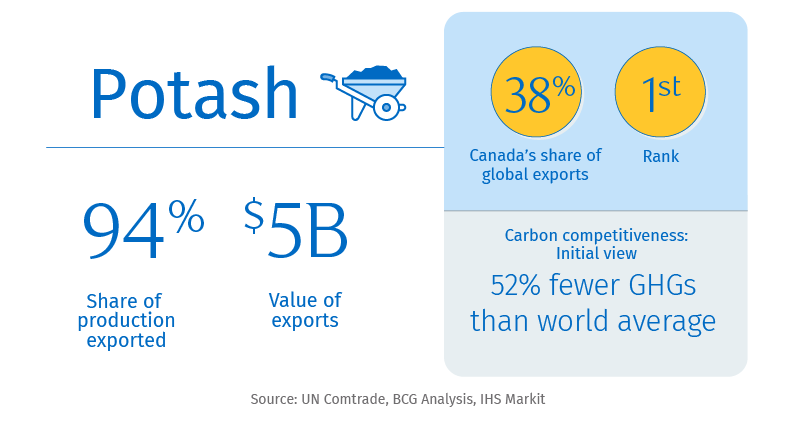

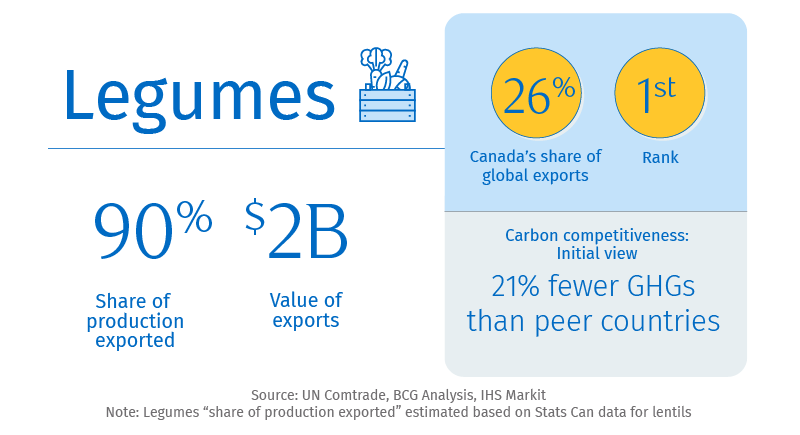

Our farmers are already among the most productive on the planet, supplying $75 billion worth of food to global markets each year. We’re a top supplier of key crops like wheat and canola and a global leader in the export of beef. We have a large stock of arable land and fresh water, a relatively stable regulatory environment, and international standing as a reliable supplier of safe, high-quality food.

But our successes have come at a cost. Every acre of food we grow, and every animal we raise, add to an emissions footprint that is already too big—and that we’ve committed to shrinking. Farming significantly more acres in the same way will only worsen the problem, since disturbing the soil adds more carbon to the atmosphere.

At the same time, climate change is battering production in many parts of the world, including Canada. But those forces may also, in the medium term, enable Canada to produce more food. This presents us with both a responsibility to help alleviate the global food crisis and an opportunity to expand our presence in international markets.

Realizing these aims will mean directing our strengths at a new target: producing significantly more food—while simultaneously slashing greenhouse gas emissions.

In this report, we identify four key steps that can set us on a path to accomplishing this. These include embracing technologies that cut emissions from fertilizer, livestock digestion and manure while also adopting farming techniques that help store carbon in soil. By leaning into its strengths, Canada can also become a leader in the development of the technologies and plant science that will power the next green revolution in agriculture.

Farmers will be on the frontlines of this transition. But they can’t do it alone. The vast number of activities involved in Canadian agriculture, the diversity of the regions in which they are carried out and the uneven distribution of emissions across them demand a national approach. To make it happen, we’ll need to harness cross-sectoral partnerships, research and innovation, policy development and private investment. We’ll need to expand the ports and railways that carry our goods to market. And we’ll have to think beyond our own borders, leading early efforts among trading partners to galvanize approaches to measurement, labelling and other mechanisms.

Canada has marshalled such an all-of-country approach to support our farmers in the past, mobilizing not just technological advances, but immigration, infrastructure and trade policies, with powerful effect.

By seizing the same spirit of collaboration now, Canadian agriculture can lead the world in the fight against climate change.

There are many different ways to analyze agricultural emissions, which different reports use to view the issue from different perspectives. Canada’s National Inventory Report (NIR) for 2019 identifies 73 megatonnes of emissions from agriculture. A full end-to-end view, including fertilizer, transport, processing, retailing, consumption and disposal, encompasses 136 megatonnes according to our analysis. We based this analysis on Environment Canada’s NIR IPCC reporting with scope 1-3 emissions assigned to operational steps in the value chain to avoid double-counting. Low magnitude and hard to influence scope 3 emissions, including manufacturing emissions of capital assets used in agriculture, were not included. One can also adjust this figure to account for exported and imported food. For import-related agricultural emissions, key import commodities were assigned emission factors per unit imported based on CONCITO databases and leveraged trading partners’ emission databases. For this paper, unless specifically noted in the text, we will define agricultural emissions as fertilizer production and use, enteric fermentation and manure management, on farm fuel use, crop residue, land use conversions and other emissions for a baseline of 93 megatonnes. We consider soil carbon sequestration to be negative emissions from farms. For potential emission reduction levers, estimates are based on current technology, economic, and operational readiness at current cost. These estimates were sized with input from published research, expert interviews, and pressure-tested based on expert judgement. There is significant uncertainty about the future impact of levers, due to both technological immaturity as well as unknowns around scope of implementation, so our lever analysis assumes some feasibility and implementation limits rather than the full theoretical scope of potential emissions reductions. We conducted preliminary analysis on the carbon competitiveness of key Canadian crops, synthesizing the results of multiple studies with varying methodologies. The initial findings are that Canadian agriculture is carbon competitive with our key export competitors; further research and refinement to carbon intensity reporting will be critical going forward.

The global challenge:

Climate change is transforming the way we grow food

Since 1961, climate change resulting from human actions slowed overall growth in global agricultural productivity by 21%.4 The story is even bleaker in warmer regions like Africa, Latin America and the Caribbean, where the growth in productivity was between 26% and 34% lower than it would have been without climate change. For many countries in the tropics, farming is set to get even harder: for every degree global temperatures rise, maize yields will fall by 7.4% and rice yields by 3.2%.

Canada won’t escape the ravages of climate change—heat, drought and extreme storms battered production as recently as 2021—but the impact will be different. By 2050, yields in parts of Canada could improve by up to 50% (as warming temperatures extend growing seasons) even as they decline by 20% to 50% in areas of China, India and the U.S.5

And as the poles warm, roughly 1.85 million square kilometres of land in Canada’s north may become suitable for staple crop production by 2080.6 With Canada losing an estimated 60,000 acres of prime farmland to urban expansion each year, there may be temptation to farm or develop it.7 But the consequences of allowing agriculture to push north could be catastrophic: releasing roughly 15 gigatonnes of carbon, if forests and wetlands are cleared and ploughed.

To feed the world, Canada will need to grow more food, without adding significantly to its stock of farmland.

Cutting emissions is key to maintaining our global agricultural might

Canada is already an agricultural superpower. The Prairies grow enough wheat to rank us among the top three exporting nations. And they churn out enough canola to dominate global markets. The mines of Saskatchewan produce and ship more critical potassium fertilizer than any other country—a billion tonnes per year. We’re among the world’s largest exporters of beef and a top exporter of lentils.

As the fifth largest source of greenhouse gas emissions, Canada’s agricultural sector is also a major contributor to the country’s carbon footprint.

Canada is a major global exporter of key agricultural commodities

Emissions intensity per kg of production (Indexed to Canadian emissions intensity)

Unleashing growth requires overcoming unique challenges

As powerful as Canada’s agricultural sector is today, significant potential remains untapped. In 2017, the Advisory Council on Economic Growth projected Canada could target an 8% global market share in agricultural products by 2027 (up from 5.7% in 2015)—making us the world’s second largest exporter after the U.S.8 As one of the few countries with the capacity to increase agricultural exports (even accounting for climate disruption), that goal appears increasingly within reach. Indeed, as new markets and trading relationships develop in response to geopolitical turbulence and climate change, more opportunities will open for major producers. Spain recently lobbied the European Commission to drop import controls on animal feed from third party countries as it struggled to address gaps left by major supplier Ukraine.9 Driven by the same shortages, as well as a desire to reduce dependence on the U.S., China is looking to accelerate imports of Brazilian corn.10

“Only a small cluster of places supply grain to the world and when you have a problem in any one of them, that loss has to be soaked up. Canada is among a narrow set of countries that has material production capacity and an exportable surplus. We’ll have all kinds of opportunities.”

Al Mussell, Research Director, Canada Agri-Food Policy Institute

But if the opportunities in agriculture’s green transformation are abundant, so too are the challenges we’ll have to manage to make it happen. They begin with the unique presence of food in our daily lives. In addition to sustaining us, food plays a central role in our celebrations, our daily rituals and our communities. As a result, changes in its availability and prices are much more visible and felt more directly by consumers. This makes change politically sensitive and difficult to carry out.

And while agriculture shares many of the challenges faced by heavy emitting, trade-exposed sectors, its pathway to reduced emissions is complicated by farm economics. Input costs are unpredictable—fertilizer expenses, for instance, increased by 31.8% in 2021 while livestock feed costs rose 23%.11 Prices for agricultural commodities, which make up the bulk of farm revenues, are among the most volatile of trade-exposed industries. And the ability to absorb these fluctuations varies widely among farm types, with profit margins on the higher end for supply-managed dairy and poultry farmers and on the lower end for beef and swine farmers who are exposed to large market swings.

Now, increasingly frequent extreme weather events—to which agriculture is more exposed than any other sector—are introducing new challenges. Amid these pressures, many farmers are reluctant to adopt new practices that add more uncertainty to their operations.12

Dairy, grain, and oilseeds are most profitable sectors

Average farm net income 2009-2019, % of revenues

Beyond the farm gate, the broader supply chain introduces its own obstacles. Canada’s agricultural sector is highly fragmented, subject to both global and regional headwinds and regulated by a patchwork of provincial and national strategies. For the most part, it is also heavily dependent on a network of rail and port infrastructure that has increasingly faced pressures, including labour shortages and disruptions due to extreme weather events. “We are in the privileged position of having all this supply that the world wants and they want it now,” said Jean-Marc Ruest, Senior Vice President, Corporate Affairs and General Counsel at Richardson International, Canada’s leading grain exporter. “But we are really struggling to get the grain out of Canada. We really need to invest in our trade infrastructure.”

The National Supply Chain Task Force has recommended a nationwide effort that brings together government and industry leaders to strengthen our transportation network against changing trade patterns, climate disruption and geopolitical risk.13 A similar approach should be brought to the challenge of lowering carbon emissions in the agricultural supply chain.

We can start by addressing three key sources of greenhouse gases in the sector—fertilizer, cattle digestion and manure. In the coming section, we’ll examine the tools that can help cut those emissions—including anaerobic digesters, carbon capture, utilization and storage (CCUS), and feed additives—as well as the challenges we face in putting them to work. We’ll also look at the potential of “regenerative agriculture” to store carbon in soil. This approach includes a set of sustainable farming practices, like reduced soil tillage and cover cropping that can also make our land more resilient to the effects of climate change.

Finally we’ll examine how our existing strengths can help us lead the research and development of new technologies that could be central to the future of farming. Together, these steps can help form the foundation of Canada’s green agricultural revolution.

Four key building blocks for a low emissions agriculture and food system

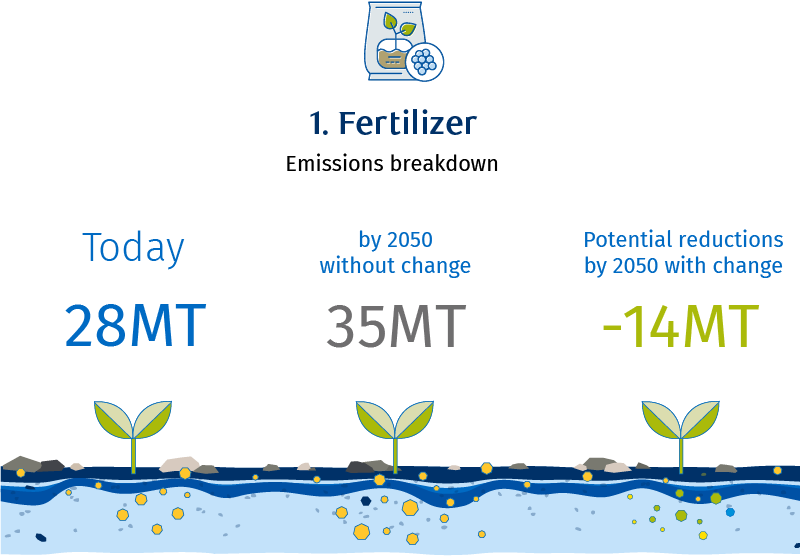

Key challenge: Fertilizer production and use produces 28MT of GHGs or 30% of our total agricultural emissions (11.9MT from production; 16MT from use)

Without change: emissions will rise to 35MT by 2050

Game changers: Use: Smart fertilizers, precision technology, nutrient stewardship. Production: carbon capture, utilization and storage (CCUS), low carbon energy feedstock

The potential: To reduce emissions by 14MT by 2050

Few places demonstrate the scale and potential of Canadian agriculture like Rob Stone’s 9,000 acre farm in Davidson, Saskatchewan. In the 1960s, Stone’s land produced 20 bushels of wheat per acre. Today, it generates 50 bushels an acre, a boost Stone credits to better plant genetics, his own farming practices and nitrogenous fertilizer.

Fertilizer use represents the single biggest input cost on Canadian farms and like many, Stone has taken steps to use it sparingly. It’s also the biggest contributor to Canada’s agricultural carbon footprint and a good place to start on our journey to a green agricultural sector.

Nitrogen feeds plants, which absorb it in their roots. Some crops, like pulses, don’t need it because they draw nitrogen from the air. But for top Canadian exports like wheat and canola, nitrogen fertilizer is essential and used on just about every field that grows them. Nitrogen fertilizer releases carbon dioxide when it’s produced and can produce nitrogenous oxide (a potent greenhouse gas with a global warming potential 265 to 298 times that of carbon dioxide over a 100-year period) when applied to fields.14,15

The good news is we have tools to reduce its use. And Canada has made progress in adopting some of them. They begin with careful planning of how fertilizer is applied on the farm. Some industry-led initiatives can assist farmers in building these plans. For instance, Fertilizer Canada’s “4R Nutrient Stewardship”, emphasizes applying the right type of fertilizer, using the right rate for application, and applying it at the right time and in the right place. Scientific assessments for Agriculture and Agri-Food Canada show the widespread adoption of some 4R practices—for example, the use of enhanced efficiency fertilizers and split application of fertilizer—could lead to significant emissions reductions.

More advanced practices, aided by data and precision technology, could take us further. On his farm in Davidson, about halfway from Saskatoon to Regina, Stone tests his soil annually, monitors yields, and uses that information to build custom plans for seeding and fertilizing at variable rates. The shift has paid off: he’s using 8 to 10% less fertilizer. The technology he uses—an air drill—also made it possible for him to plant his crops without tilling the soil, a practice that improves soil quality and increases productivity by reducing the need to rest land in alternate years.

Cutting emissions from fertilizer production involves solutions at a much larger, industrial scale. Carbon capture, utilization and storage systems (CCUS), which are beginning to be used in the oil and gas sector, capture emissions before they enter the atmosphere and compress them into a liquid that’s shipped by pipeline to a storage facility. Saskatoon-based Nutrien is now using such a system to capture carbon dioxide from its Redwater plant and move it via the Alberta Carbon Trunk Line to enhanced oil recovery projects in central Alberta. Another option being explored is the process of electrolysis, which produces fertilizer by using renewable electricity to draw hydrogen from water.

The challenges: Many Canadian farms are small and operate on thin margins that make absorbing the cost of soil testing and precision agricultural technology difficult. A recent RBC survey of 200 Canadian farmers, found that those with lower annual revenues ($250,000 to $999,000) were less likely than those with higher-revenues to be using environmentally sustainable farming practices. (However, nearly all lower revenue farms that have not yet adopted green farming practices are planning to do so in the near future). Just 13% of farmers across Canada are using variable rate techniques on their farms.16 And though the number is rising, less than a third of farmers are currently testing soil for nutrients on an annual basis—a starting point for more efficient fertilizer use.

For farmers, the risk of change is also a challenge. Research shows many producers are reluctant to adopt practices that introduce uncertainty to their operations. “These are family farms,” said Don Smith, Vice President, Petroleum and Innovation at United Farmers of Alberta. “They’re not going to experiment with new technologies if there’s a risk it could negatively impact their ability to feed their family.”

Cost and uncertainty are barriers on the production side too. Beyond Nutrien’s Redwater facility, only a minor fraction of fertilizer production employs CCUS. Though costs vary by facility, the estimated capital cost of this technology can be up to $50 million per plant depending on facility size and location, with barriers to investment including uncertainty about regulatory approvals and carbon pricing17. What’s more, CCUS is heavily dependent on infrastructure that requires further development, including carbon pipelines and storage hubs.

“The most cost effective, immediately available technology is carbon capture and storage. But it is capital intensive.”

Clyde Graham, Executive Vice President, Fertilizer Canada

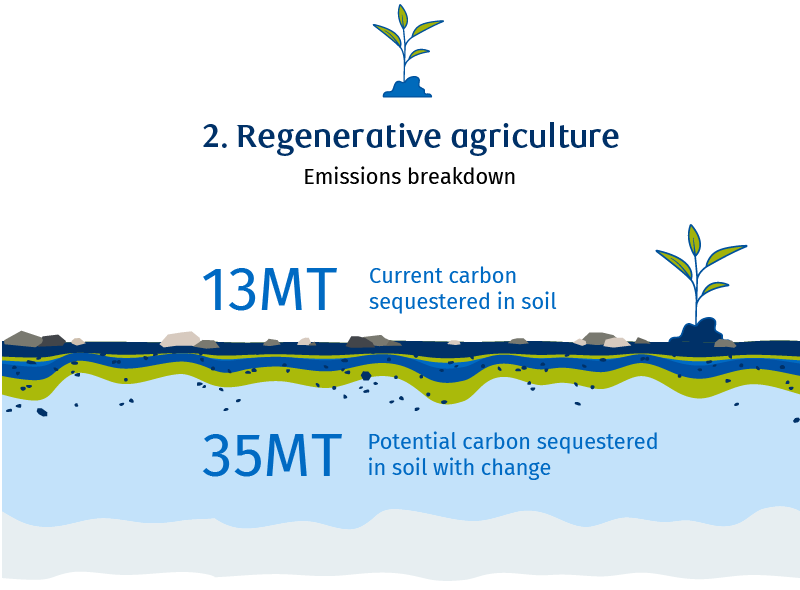

Current carbon sequestered in soil: 13MT

Game changers: Agroforestry, biochar, alley cropping, silvopasture, conservation and no-till practices, cover cropping, avoided land use conversion

The potential: Negative emissions rising up to 35MT

When it comes to growing food, soil is our most precious resource. About 95% of the world’s food is grown in the uppermost layer of topsoil—more than half of which has disappeared in the last 150 years due to modern, intensive farming practices. Without change, the consequences of losing even more soil will be severe. The earth’s ability to grow food and absorb water plummets without healthy topsoil, leaving us more vulnerable to both hunger and flooding.

Soil performs another vital service: it stores carbon. Indeed, while agriculture is one of the key contributors to emissions, it also holds enormous power to act as a “carbon sink,” removing carbon from the atmosphere where it contributes to climate change. Modern farming practices, like tilling, can impair this important function by disturbing the carbon in soil.

Investing in our soil then, is a critical early step in establishing a green agriculture sector. “Regenerative agriculture” aims to do this through a holistic approach to farming intended to improve soil health, protect biodiversity and draw greenhouse gases out of the atmosphere and into the ground. Though the term first appeared in the 1980s, it gained traction following a 2014 paper by the non-profit Rodale Institute, which outlined how certain soil-friendly farming techniques could sequester carbon in soil. It’s since become a top food trend in the U.S., where a growing range of products feature it as a credential and where companies like General Mills, PepsiCo and Nestle have announced commitments to advancing regenerative agriculture on millions of acres of farmland. In Canada, companies including McCain Foods, Maple Leaf Foods, Nutrien and McDonald’s Canada have launched similar initiatives.

Broadly speaking, regenerative agriculture refers to a set of practices, including reducing or eliminating soil tillage, planting cover crops (which prevent erosion and improve fertility) and furthering animal grazing techniques (which give land time to regenerate and improve the soil’s ability to store carbon).

Many Canadian farmers already use these regenerative agriculture practices. About 60% of farmers use no-till or conservation tillage practices, for example. In Saskatchewan, that figure is even higher at 80%. Adoption of other practices could take us further. Cover cropping has the potential to mitigate 9.6MT of emissions, according to the non-profit Nature United. And biochar, which turns agricultural waste into a soil enhancer that can hold carbon, could cut 6.8MT. But adopting practices that draw greenhouse gasses out of the atmosphere is only part of the equation. We also need to prevent future emissions from happening in the first place. One way to do this is by protecting grasslands, which currently trap a huge amount of carbon. Preventing grasslands from being ploughed up or paved over could mitigate 12.4MT of carbon emissions in Canada.

Many of these practices—which are now under the banner of regenerative agriculture—have long been used by Indigenous communities. And these communities have much knowledge to share as we explore the potential of these techniques.

“It’s what we’ve done all along and it’s the opposite of primitive. It’s about resilience and adaptation. You can push the land but you have to also invest, not squeeze every last drop out of it.”

Jennifer Grenz, Assistant Professor, University of British Columbia

The challenges: Greater adoption of regenerative agriculture has been hindered by financial concerns among farmers. The cost of adopting it varies per acre across practices. And upfront investments in enabling equipment like air seeders can also be prohibitive. Producers—particularly those with slim profit margins—typically need assurances that returns will cover those costs and the risks associated with them. But according to our research, the benefits of some of these practices generally only begin to outstrip the costs four years after their adoption. And profitability appears only in year six. Meantime, markets to compensate farmers for storing carbon in soil—as well as the methods to measure it—are still in experimental stages and generally lack a sufficient payout to make up the for the upfront investment.

Uncertainty presents another, critical barrier. Regenerative agriculture lacks a single legal or regulatory definition and there is no oversight for how it’s used. This leaves it open to misuse and bold claims about its power to store carbon, when much of that is still open to scientific debate. With no single test or certification for claims, farmers (and consumers) are left to sort out credibility on their own.

Soil carbon sequestration is key to cutting emissions

Million tonnes of CO2 equivalent

Defining the term and creating a system to measure, report and verify (MRV) the carbon stored in soil due to regenerative agriculture (and the ecosystem services provided), would empower consumer choices. An MRV tool would also make it easier to attach a price to practices and lead to a market where carbon credits can be bought and sold. Some pilot projects are underway to create “carbon farms” that include attempts to build accurate MRV systems. Other projects are experimenting with advanced mathematical models that estimate how different farm management strategies may sequester carbon.

Whatever system is established will need to address myriad regional variations in soil types across the country, as well as limitations related to farming type and size. Creating a nationwide MRV accounting tool will also require a much broader system for soil testing than Canada currently has. Technology, and in particular the advancement of remote soil sensors, will be critical enablers of these systems.

Answers to these questions and others—including how to regulate future carbon markets—will take time to come together. Until then, we’ll need to find ways to incentivize farmers using the best tools we have, while consistently adopting better ones as they arise.

“We couldn’t produce without cover crops. Crazy storms used to wipe out our crops. Not anymore.”

Gillian Flies, Owner, The New Farm

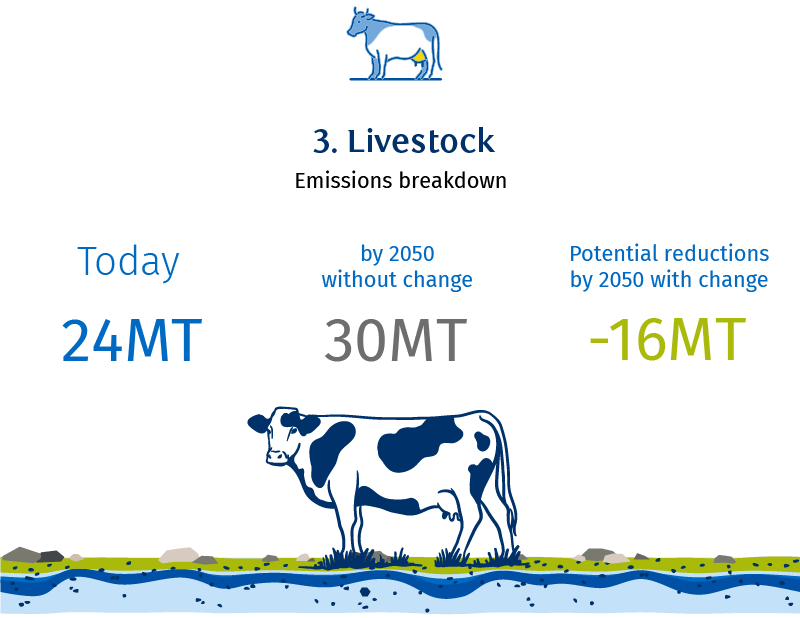

Key challenge: Cattle digestion produces 24MT of emissions

Without change: Emissions will rise to 30MT by 2050

Game changers: Feed additives, GHG selective breeding

The potential: To reduce emissions by 16MT by 2050

Cow burps and manure may not immediately spring to mind when we think about climate change. But Canada’s dairy and beef cattle are the biggest sources of agricultural emissions after fertilizer. Through their digestion process or “enteric fermentation”, cattle produce methane, a potent greenhouse gas with a 20 year global warming potential 85 times that of carbon dioxide.18 And in Canada, where the agricultural sector accounts for 30% of national methane emissions, 85% can be directly attributed to cattle.19

The paradox is that cattle can also act as stewards of the land. Canada has about 35 million acres of native grassland and nine million acres of seeded grasslands that act as carbon sinks. By grazing on this land, cattle stimulate grass roots to grow deeper, better enabling carbon to be stored in the soil. Using land for grazing also prevents it from being converted to other uses, which impacts biodiversity and disturbs carbon in the soil.

Adding to the complexity, Canadian beef has one of the smallest carbon footprints globally, with greenhouse gas emissions well below the global average. That makes us a critical beef supplier as the world looks to cut emissions. Our dairy cattle too, emit fewer GHGs per kilogram of final product than the global average.

Still, the outsized contribution of cattle to climate change means more must be done. Researchers are working on breeding techniques that could produce cattle that release less methane and that process feed more efficiently. Feed additives that cut the amount of methane produced during digestion could offer a more immediate breakthrough for the sector. One such additive, called 3NOP, is already in use in other countries—it has yet to be approved in Canada—and has been shown to cut emissions by as much as 45%.20 Adding seaweed to the diet of dairy cows could also cut emissions by as much as 82% while also improving the efficiency of cattle—that is, helping them grow more using less feed.21

The challenge: Feed is the most expensive and most critical input on a beef or dairy farm and questions remain about how much additives will cost amid strong international demand. A more practical concern is how to administer the additives to beef cattle that spend much of their lives grazing in open fields (where the most emissions are released).

“Feed additives are a hard sell. As we have learned working with veterinarians and feedlot operators, basically there’s no incentive…And ultimately we’re depending on the unknown: the adoption of the farmer.”

Elena Vinco, Researcher and Policy Analyst, The Simpson Centre for Food and Agricultural Policy

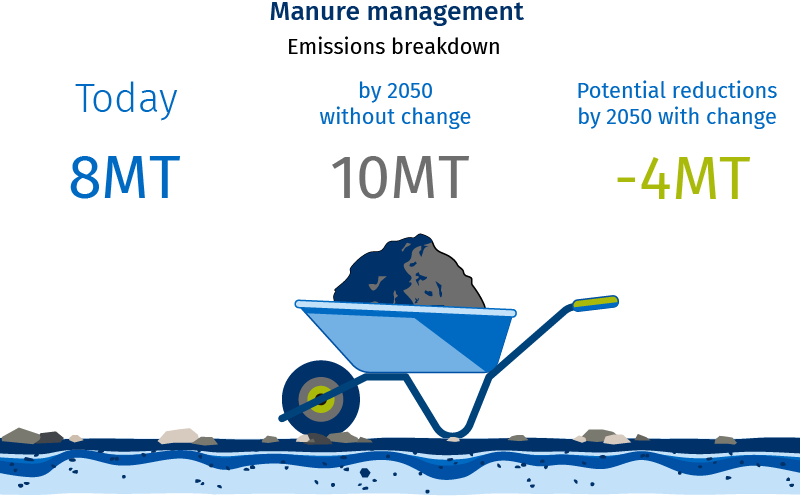

Key challenge: Manure produces 8MT of emissions

Without change: Emissions will rise to 10MT by 2050

Game changer: Anaerobic digesters

The potential: To reduce emissions by 4MT by 2050

While less potent than cow burps, manure packs a major punch when it comes to emissions. Today, 8MT of total agricultural emissions come from manure. Of this, 55% are generated by cattle.

Walker Farms in Aylmer, southeast of London, Ontario, offers a glimpse at one way to bring those emissions down—while adding to the farm’s bottom line. The dairy operation partnered with Ontario-based DLS Biogas to build a $16 million anaerobic digester, technology that turns manure and organic waste into electricity or renewable natural gas (RNG). Farmers can either use that energy on the farm, cutting their own costs, or sell it to natural gas utilities like Fortis B.C. under long-term contracts. Fortis buys the gas and the carbon credits associated with it.

Digestate, an odourless byproduct, can in turn be used as fertilizer. Canada currently has 279 biogas projects in operation. And with only 13% of available biogas energy production being tapped in Canada, there’s room to grow, with the most significant potential identified in the agricultural sector.22

The challenges: Anaerobic digesters are gaining traction, largely due to the extra revenue they bring to farms. The Walkers expect to see their initial investment returned in eight years.

But the upfront cost of digesters—running anywhere from $7 million to $70 million—place them out of reach for smaller operators. The Walkers and DLS Biogas have applied for a series of grants (a process that took hundreds of hours to complete) but there are no guarantees and no programs specifically tailored to biogas.

And digesters may not make sense for every farm. With at least 150 cows needed to produce enough manure to feed a digester (Ontario averages 70 to 80 cows per farm), size matters. Access to landfilled food waste, which is also added to digesters, and pipelines to move the RNG to market are also critical. Large beef feedlots in Alberta tend to have better access to this infrastructure and enough cattle to make production economically viable. But the clay surface used in many cattle pens can end up in manure, damaging biodigester machinery. Many feedlots are converting to roller compacted concrete, which improves cattle efficiency and eliminates the problem of clay in the biogas process. This, too, is costly.

The development of communal digesters could allow smaller farms to participate in the production of biogas. But support to help cover the upfront costs—and a streamlined process to obtain it—will be critical.

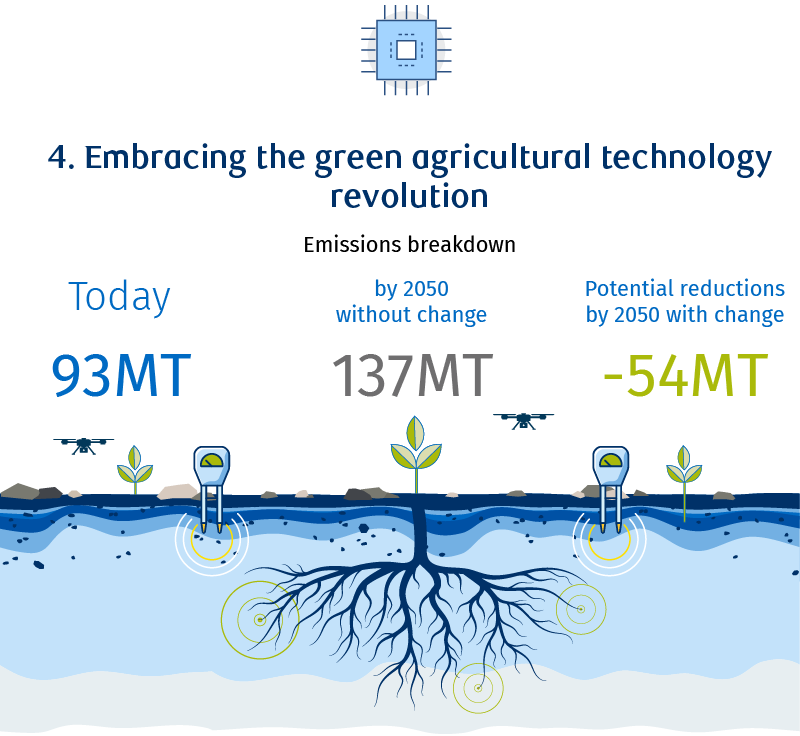

Key challenge: 93 MT overall

Without change: 137 MT

Game changers: Advanced ag-tech that cuts emissions, enables more carbon to be stored in soil and leads to more production on less land

The potential: To enable 54 MT in potential emissions reductions (or as much as 76 MT when soil sequestration is added)

Canada has a long history of agricultural innovation. The development of Marquis Wheat in 1904 was vital to the boom in Prairie crop yields that followed. Canola, created in Saskatchewan in the 1960s, is now one of the world’s most important oilseed crops. The grain auger was invented in Canada. And air seeders bearing the logo of Saskatchewan’s Seed Hawk can now be found on fields from Australia to Europe.

All of these developments fueled step changes in the productivity of Canadian agriculture. The next generation of technologies will need to do more than that. Indeed, all of the emissions reductions envisioned in this paper will in some way rely on technology—innovations like CCUS, biodigesters and precision tools. Technology will also be critical to producing more food on less land and by extension, avoiding the conversion of land into cropland. Our estimates suggest we can avoid 20MT of emissions by preventing land use change between now and 2050. Storing more carbon in soil—producing negative emissions—will also depend on increasingly sophisticated devices like soil sensors and drones that enable the market innovation necessary to accelerate new approaches like regenerative agriculture.

Canada’s heft in global agriculture markets, its longstanding expertise in crop science and its newfound strength in artificial intelligence and data science, position us well to lead in some areas of this race. Yet when it comes to drawing private investment to homegrown innovation, we’re falling behind. Of roughly US$36 billion in global venture capital and private equity investments in ag-tech since 2017, Canada received just 3%, or US$1 billion. The U.S. captured US$20 billion or 55% of investments.

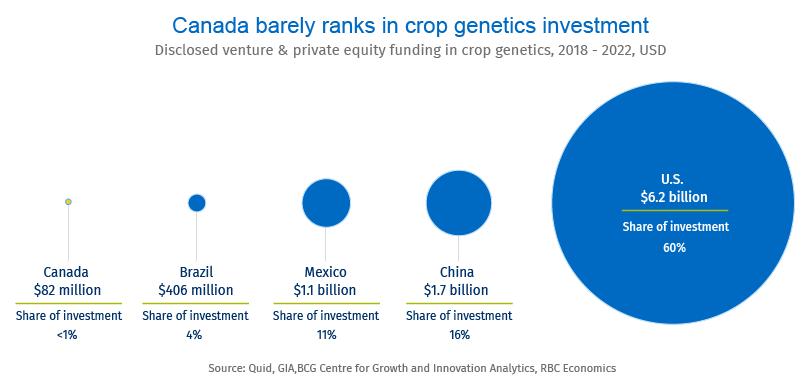

Critically, private equity and venture capital investment has lagged in some of the areas that have historically reaped the largest rewards for Canadian agriculture. As we look to lower emissions, crop genetics and soil science (including microbiome research) hold some of the greatest potential for boosting production on existing farmland, cutting carbon emissions and improving resilience to droughts and flooding. While much of our research has been focused “above the soil” in the past, scientists are increasingly turning their attention to the potential of root structures and soil microbiomes to cut emissions. But so far, private investment in these fields hasn’t rushed to Canada. Of total global private equity and venture capital investment of roughly US$10 billion since 2017, our ventures in crop genetics have drawn only US$82 million.

In addition, much of the investment Canada is attracting isn’t going to the kinds of technologies we need now to transition to a more sustainable agriculture and food sector. Globally, over half of private investment in ag-tech in 2021 was in sustainable practices. But in Canada, most investments are focused on digitization and automation, technology designed with productivity, not sustainability, in mind.

As we work to deploy these solutions today we’ll also need to keep an eye to the future, investing in earlier stage technologies that can help us adapt our food systems to climate change. “Controlled environment” agriculture, such as greenhouses and vertical farms that allow crops to be grown indoors and in stacked layers, is taking off around the world. Canada currently imports fresh produce at a low cost from regions that are far more vulnerable to climate change. Tech-based alternatives like these could help us maintain domestic food security in an increasingly volatile world of climate and political disruptions. Meantime, cellular agriculture and precision fermentation technologies, which are advancing rapidly, could increasingly provide consumers with alternatives to meat and dairy products.

“I think plant breeding could really do it for us. If you look at all the advances we’ve made in higher yields, disease, resistance, all these kinds of traits and that’s all been focused above ground. There’s an equal opportunity below ground to make all kinds of significant advancements.”

Stuart Smyth, Associate Professor, College of Agriculture and Bioresources, University of Saskatchewan

The challenges: Artificial intelligence and data science, engineering, the “Internet of Things”, including sensors and drones, as well as biotechnology, are critical to the development of modern ag-tech. So are the skills that go with them. Yet efforts to draw this specialized talent and develop these skills among youth have fallen short of our needs.

Most support for Canadian research comes from public funding—which has been behind many of our successes. Marquis Wheat, which dramatically improved yields in the Prairies in the early 1900s, was developed through Dominion Experimental Farms—a system of stations, operated by the federal government, which investigated agricultural problems and created new techniques to assist farmers. Current funding programs can be onerous for researchers, particularly for emerging technologies that don’t fall easily into specific funding categories. And certain regulatory requirements—including those surrounding novel plant traits—can act as barriers to approval and investment in emerging areas of plant science like gene editing.

While Canadian researchers continue to rely on public investment, other countries including the U.S., are seeing most of their overall research dollars come from the private sector. Competing in the next era of agriculture will depend on our ability to mobilize more of this capital.

Fighting food waste

Emissions arise not just from the food we grow but from the food we waste. In Canada, 58% of the food produced for human consumption is wasted or lost along the supply chain, of which 18% could be avoided.23 The economic cost of all that waste is $49 billion a year—a figure that climbs even higher when lost labour, transportation and other factors are accounted for.

Though a lot of waste happens during production and processing, just 14% of that is avoidable. Technological advancements have done much to eliminate food loss at the production stage, an effort driven in part by the cost savings it generates.

Among consumers, the problem of food waste is far more entrenched. Studies suggest 18% of all food produced is wasted in ways that could be avoided. Almost half of that avoidable waste comes from hotels, restaurants and households, with consumers in wealthier countries far more likely to waste food than those in poorer countries. As that food decomposes in landfills, it releases greenhouse gases, as much as 12 MT—when measured from end-to-end.

Solving the problem of consumer food waste means tackling a cluster of causes. These include time scarcity (consumers lack the time they need to plan meals and use food before it goes bad); a lack of education on how to prevent food waste through more thoughtful storage and use of cooking waste like vegetable stalks; and retail promotions that encourage consumers to buy more than they need.

In addition to cutting food loss, industry has done much to extend the shelf life of food through packaging and other controls. More novel packaging solutions are underway that use plant-based and microbial packaging and coating solutions to do the same. Sensors can tell us when food has actually spoiled rather than leaving consumers to rely on best before dates. And new business models are emerging, such as those that transform food that doesn’t meet retail standards into poultry feed and other uses.

But ultimately, solving the problem of food waste will depend on us.

Recommendations: Seeding change

Cutting our greenhouse gas emissions, while also meeting our responsibility to feed the world, is a challenge rife with uncertainty. With many agricultural technologies and farm practices still in nascent stages, and widespread adoption still elusive, questions will continue to hang over our actions.

This risks paralyzing our efforts at a time when there isn’t time to lose. The stakes of the current food crisis are staggering: shortages and high prices for staple goods, have put the lives and livelihoods of 345 million people in immediate danger of acute food insecurity.24 Low income countries, many of which depend on imports from Ukraine and Russia, including Somalia, South Sudan and Yemen, are among the most vulnerable. In North America and other higher income countries, soaring food prices due to shortages and post-pandemic inflation are also dominating public agendas.

The urgency of the situation means we’ll need to act boldly using the best tools we have today. And we’ll need to do it together. Policymakers, private businesses and producers will need to collaborate in new ways as we pursue a national strategy designed to support farmers. This begins by focusing on the building blocks we’ve identified above, and on the key pillars of technology, people, policy, and economics. Working with BCG Centre for Canada’s Future and the Arrell Food Institute, we’ll explore each of these pillars in depth in the coming months.

Building an agricultural sector fit for an age of climate disruption is a challenge unlike any we’ve faced. But few countries are better positioned than Canada to confront it.

The global threat of food insecurity growing. So, too, is our ability to lead a new age of innovation to both harvest our land and sustain it.

Planting a paradigm shift: Building the 4 key pillars of a low emissions food strategy

Policy

Establish a national plan for a low-emissions agriculture sector. Our plan for cutting emissions must take all stakeholders into account and rally not just farmers, but investors, private business and Canadians. Producing food more sustainably will mean making tough choices and supporting investment in key technologies, like carbon capture, utilization and storage (CCUS). It will also mean doing a better job of marketing Canada’s sustainable food to the world.

Lead efforts to create global alignment on a low-emissions food standard. Roughly 61% of our agricultural emissions are tied to goods that are ultimately exported. Advancing an emissions reduction strategy that’s misaligned with our key export markets could create friction in our trading relationships. We need to align trading partners around a common set of goals, indicators and GHG measurement, reporting and verification protocols. Canada, a longstanding supporter of free trade, and a global leader in multilateral processes, can lead these efforts.

Integrate agricultural strategies with energy strategies. Farmers are increasingly embracing opportunities to generate renewable natural gas from their operations. Integrating these efforts with a national energy strategy could help accelerate the deployment of clean energy both on and off the farm.

Technology

Create a central funding body for research and development, operating in close partnership with academia and the private sector. Many of the most promising and advanced areas of Canadian agricultural research don’t fit within current funding categories. A more centralized system such as in the United States Department of Agriculture, could develop a more holistic, nationwide view of where support and innovation is needed. The leadership shown by federal governments in creating the innovation super clusters provides a playbook for how Canada can super charge agri-food research and innovation.

Focus on technologies that hold the most promise to cut emissions. As we target funding to technology that accelerates productivity, we need to also attract more investment to technologies that cut emissions from key drivers in the supply chain—innovations like anaerobic digesters, feed additives and CCUS. Funding should also be focused on those technologies that enable sustainable practices to be adopted and rewarded, like soil sensors, and precision technologies.

Create innovative tax and financial incentives to spur more private investment. Accelerating private investment in Canadian agtech will mean thinking more creatively about the tax and financial incentives we have in place. We need to encourage the automation that will be key to our agricultural productivity and international competitiveness—and that will draw more capital to the technologies that will drive the future of low emissions farming. Expanding accelerated depreciation beyond tangible assets to include artificial intelligence and other agtechs is one possibility.

Economics

Make it pay. Forcing farmers to pay for emissions they already produce could add pressure to high food prices. A better approach is to compensate farmers for reducing them. Yet existing models like carbon credits are insufficient and place an unequal burden on the farmer. A national standard for measuring the impact of emissions-cutting activities, including a mechanism for measuring, reporting and verifying (MRV) carbon stored in soils, could be critical to compensating farmers and to empowering policymakers and financial institutions to mobilize support. This standard—also key to attracting investment—will need to be designed and regulated on a national basis and aligned internationally with our major trading partners.

Share the risk. For farmers, the adopting of emissions-cutting technology adds more uncertainty to a business already weighted with risk. Governments and other companies in the agricultural value chain have an important role to play in sharing the risk burden. That’ll mean insuring against yield losses for farmers who adopt sustainable practices. For example, right now there is no incentive for sustainable agriculture under crop insurance schemes though these practices are proven to reduce the impact of flooding and drought. Crop insurers should be willing to adjust premiums to reflect these shifting risks.

People

Build the skills. Leverage the Labour Market Information Council to pinpoint the skills farmers need to shift toward a more resilient food system. As we’ve noted in previous research, digital skills will be critical to the future of food production.25 So too will knowing how to apply tools in ways that cut emissions. Beyond data and technology, some farmers will need support to employ regenerative agriculture techniques and other tools on the farm. Experiential learning platforms including hands-on mentorship and co-op programs can accelerate this transition.

Broaden the talent pool. The lack of awareness about the potential for a fulfilling career in agriculture has hampered recruitment of individuals with the coding, artificial intelligence and data science skills critical to the future of food. Yet few sectors hold greater potential for innovation than agriculture. Educating students on the opportunities in the field—through co-ops, outreach and liaison programs—will be critical to bringing their talents to the challenge.

For more, go to rbc.com/climate.

Download the Report

\

Contributors:

RBC

Naomi Powell, Managing Editor, Economics and Thought Leadership

John Stackhouse, Senior Vice President

Colin Guldimann, Economist

Farah Huq, Senior Director, Content Strategy

Darren Chow, Senior Manager, Digital Media

Trinh Theresa Do, Senior Manager, Thought Leadership Strategy

Zeba Khan, Manager, Digital Publishing

Aidan Smith-Edgell, Research Associate

Kitty Wu, Intern

Gwen Paddock, Director, Sustainability & Climate – Agriculture

Ryan Riese, National Director, Agriculture

Boston Consulting Group

Keith Halliday, Director, Centre for Canada’s Future

Kilian Berz, Managing Director and Senior Partner

Shalini Unnikrishnan, Managing Director and Partner

Sonya Hoo, Managing Director and Partner

Chris Fletcher, Managing Director and Partner

Thomas Foucault, Managing Director and Partner

Wendi Backler, Partner and Director, BCG Centre for Growth and Innovation Analytics

Kate Banting, Head of Marketing and Social Impact

Simon Beck, Principal

Youssef Aroub, Project Leader

Ilana Hosios, Consultant

Anguel Dimov, Consultant

Pilar Pedrinelli, Consultant

Zahid Gani, Consultant

Rachel Ross, Consultant

Rachit Sharma, Lead Knowledge Analyst, BCG Centre for Growth and Innovation Analytics

Arrell Food Institute, University of Guelph

Evan Fraser, Director

Margarita Fontecha, Arrell Food Institute Scholar, Ph.D. Candidate, Environmental Design and Rural Development

Laura Hanley, M.Sc. Student, Food Science

Ibrahim Mohammed, Ph.D. Candidate, Environmental Sciences

Deus Mugabe, Ph.D. Candidate, Plant Agriculture

Brenda Zai, M.Sc. Student, Food Science

Dr. Krishna KC, Research Scientist

Dr. Jesus Pulido-Castanon, Post-doctoral Research Associate

Emily Duncan, PhD Candidate

1. This figure does not include downstream processing, transportation, retail or food service operations. See methodology.

2. See methodology.

3. World Population Growth – Our World in Data

4. Anthropogenic climate change has slowed global agricultural productivity growth | Nature Climate Change

5. World Economic Forum (weforum.org)

6. Opportunities and trade-offs for expanding agriculture in Canada’s North: an ecosystem service perspective (facetsjournal.com)

7. Why You Should Care About Farmland Loss – Canadians for a Sustainable Society

8. key-sectors-secteurs-cles-eng.pdf (budget.gc.ca)

9. UPDATE 1-Spain lobbying European Commission to buy emergency corn from Argentina | Reuters

10. China Set to Import Brazilian Corn in Challenge to US Supply – Bloomberg

11. The Daily — Farm income, 2021 (statcan.gc.ca)

12. Climate Change Is Hitting Farmers Hard – Scientific American

13. Act. Collaboration. Transformation. Final Report of the National Supply Chain Task Force 2022 (canada.ca)

14. Fifth Assessment Report — IPCC

15. Global Warming Potentials (IPCC Fourth Assessment Report) | UNFCCC

16. SPARK-FERTILIZER-USE-IN-CANADA-REPORT-2022-VF_08_04_2022.pdf (fertilizercanada.ca)

17. CCUS-Strategy_Template-for-Input_Fertilizer-Canada-Response_Final_March-2022-combined.pdf (fertilizercanada.ca)

18. In other words, over 20 years, one gram of methane produces 85 times the amount of warming as a gram of carbon dioxide.

19. Home Page – Simpson Centre

20. Home Page – Simpson Centre

21. Red seaweed (Asparagopsis taxiformis) supplementation reduces enteric methane by over 80 percent in beef steers | PLOS ONE

22. Canada’s 2020 Biogas Market Report : Canadian Biogas Association

23. The Avoidable Crisis of Food Waste: Technical Report (secondharvest.ca)

24. Global Food Crisis Demands Support for People, Open Trade, Bigger Local Harvests (imf.org)

25. Farmer 4.0: How the Coming Skills Revolution Can Transform Agriculture – RBC Thought Leadership

In addition to those cited in this report, we’d like to thank the following individuals for their insights:

- Katie M. Wood, Associate professor, Ruminant Nutrition and Physiology, University of Guelph

- Lisa Ashton, PhD Candidate, University of Guelph

- Lenore Newman, Canada Research Chair in Food Security and the Environment and Professor of Geography, Simon Fraser University

- Dennis Laycraft, Executive Director, Canadian Cattle Association

- Brenna Grant, Executive Director, Canfax Research Services

- Mark Thompson, Executive Vice President, Chief Corporate Development and Strategy Officer, Nutrien Ltd.

- Michelle Nutting, Director, Agricultural and Environmental Sustainability, Nutrien Ltd.

- Dan Heaney, Research Associate, Plant Nutrition Canada

- Tom Steve, General Manager, Alberta Wheat Commission

- Jason Lenz, Vice President, Alberta Wheat Commission

- Dan McCann, CEO, Precision AI

- Daniel Brisebois, Ferme Coopérative Tourne-Sol

- Juanita Moore, Vice President of Corporate Development, GoodLeaf Farms

- Janay Meisser, Director of Innovation, United Farmers of Alberta

- Les Wall, CEO, KCL Cattle Company

- Kate Parizeau, Associate Professor, Department of Geography, Environment, and Geomatics, University of Guelph

- Tammara Soma, Assistant Professor, School of Resource and Environmental Management (Planning), Simon Fraser University

- Mauricio Alanís, Director, Sustainability Strategy and Partnerships, Maple Leaf Foods

- Ryan Phillippe, Director, Corporate Development, Genome Canada

- Josh Bourassa, Research Associate, The Simpson Centre for Food and Agricultural Policy

- Guillaume Lhermie, Director, The Simpson Centre for Food and Agricultural Policy

- Lejjy Gafour, President, Cult Food Science Corp.

- Jane Church, Corporate Engagement Manager, Nature United

- Tony Ward, Professor Emeritus, Department of Economics, Brock University

- Tyson Kamminga, Chief Financial Officer, Kroeker Farms Limited

- Wayne Rempel, CEO, Kroeker Farms Limited

- Brian Gilvesy, CEO, ALUS

- Dave MacMillan, CEO, Deveron UAS

- Derek Eaton, Director of Public Policy Research and Outreach, Smart Prosperity Institute

- David Hughes, President and CEO, The Natural Step Canada

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

Without change: emissions will rise to 35MT by 2050

Game changers: Use: Smart fertilizers, precision technology, nutrient stewardship. Production: carbon capture, utilization and storage (CCUS), low carbon energy feedstock

The potential: To reduce emissions by 14MT by 2050

Game changers: Agroforestry, biochar, alley cropping, silvopasture, conservation and no-till practices, cover cropping, avoided land use conversion

The potential: Negative emissions rising up to 35MT

Defining the term and creating a system to measure, report and verify (MRV) the carbon stored in soil due to regenerative agriculture (and the ecosystem services provided), would empower consumer choices. An MRV tool would also make it easier to attach a price to practices and lead to a market where carbon credits can be bought and sold. Some pilot projects are underway to create “carbon farms” that include attempts to build accurate MRV systems. Other projects are experimenting with advanced mathematical models that estimate how different farm management strategies may sequester carbon.

Whatever system is established will need to address myriad regional variations in soil types across the country, as well as limitations related to farming type and size. Creating a nationwide MRV accounting tool will also require a much broader system for soil testing than Canada currently has. Technology, and in particular the advancement of remote soil sensors, will be critical enablers of these systems.

Answers to these questions and others—including how to regulate future carbon markets—will take time to come together. Until then, we’ll need to find ways to incentivize farmers using the best tools we have, while consistently adopting better ones as they arise.

“We couldn’t produce without cover crops. Crazy storms used to wipe out our crops. Not anymore.”

Gillian Flies, Owner, The New Farm

Key challenge: Cattle digestion produces 24MT of emissions

Without change: Emissions will rise to 30MT by 2050

Game changers: Feed additives, GHG selective breeding

The potential: To reduce emissions by 16MT by 2050

Cow burps and manure may not immediately spring to mind when we think about climate change. But Canada’s dairy and beef cattle are the biggest sources of agricultural emissions after fertilizer. Through their digestion process or “enteric fermentation”, cattle produce methane, a potent greenhouse gas with a 20 year global warming potential 85 times that of carbon dioxide.18 And in Canada, where the agricultural sector accounts for 30% of national methane emissions, 85% can be directly attributed to cattle.19

The paradox is that cattle can also act as stewards of the land. Canada has about 35 million acres of native grassland and nine million acres of seeded grasslands that act as carbon sinks. By grazing on this land, cattle stimulate grass roots to grow deeper, better enabling carbon to be stored in the soil. Using land for grazing also prevents it from being converted to other uses, which impacts biodiversity and disturbs carbon in the soil.

Adding to the complexity, Canadian beef has one of the smallest carbon footprints globally, with greenhouse gas emissions well below the global average. That makes us a critical beef supplier as the world looks to cut emissions. Our dairy cattle too, emit fewer GHGs per kilogram of final product than the global average.

Still, the outsized contribution of cattle to climate change means more must be done. Researchers are working on breeding techniques that could produce cattle that release less methane and that process feed more efficiently. Feed additives that cut the amount of methane produced during digestion could offer a more immediate breakthrough for the sector. One such additive, called 3NOP, is already in use in other countries—it has yet to be approved in Canada—and has been shown to cut emissions by as much as 45%.20 Adding seaweed to the diet of dairy cows could also cut emissions by as much as 82% while also improving the efficiency of cattle—that is, helping them grow more using less feed.21

The challenge: Feed is the most expensive and most critical input on a beef or dairy farm and questions remain about how much additives will cost amid strong international demand. A more practical concern is how to administer the additives to beef cattle that spend much of their lives grazing in open fields (where the most emissions are released).

“Feed additives are a hard sell. As we have learned working with veterinarians and feedlot operators, basically there’s no incentive…And ultimately we’re depending on the unknown: the adoption of the farmer.”

Elena Vinco, Researcher and Policy Analyst, The Simpson Centre for Food and Agricultural Policy

Key challenge: Manure produces 8MT of emissions

Without change: Emissions will rise to 10MT by 2050

Game changer: Anaerobic digesters

The potential: To reduce emissions by 4MT by 2050

While less potent than cow burps, manure packs a major punch when it comes to emissions. Today, 8MT of total agricultural emissions come from manure. Of this, 55% are generated by cattle.

Walker Farms in Aylmer, southeast of London, Ontario, offers a glimpse at one way to bring those emissions down—while adding to the farm’s bottom line. The dairy operation partnered with Ontario-based DLS Biogas to build a $16 million anaerobic digester, technology that turns manure and organic waste into electricity or renewable natural gas (RNG). Farmers can either use that energy on the farm, cutting their own costs, or sell it to natural gas utilities like Fortis B.C. under long-term contracts. Fortis buys the gas and the carbon credits associated with it.

Digestate, an odourless byproduct, can in turn be used as fertilizer. Canada currently has 279 biogas projects in operation. And with only 13% of available biogas energy production being tapped in Canada, there’s room to grow, with the most significant potential identified in the agricultural sector.22

The challenges: Anaerobic digesters are gaining traction, largely due to the extra revenue they bring to farms. The Walkers expect to see their initial investment returned in eight years.

But the upfront cost of digesters—running anywhere from $7 million to $70 million—place them out of reach for smaller operators. The Walkers and DLS Biogas have applied for a series of grants (a process that took hundreds of hours to complete) but there are no guarantees and no programs specifically tailored to biogas.

And digesters may not make sense for every farm. With at least 150 cows needed to produce enough manure to feed a digester (Ontario averages 70 to 80 cows per farm), size matters. Access to landfilled food waste, which is also added to digesters, and pipelines to move the RNG to market are also critical. Large beef feedlots in Alberta tend to have better access to this infrastructure and enough cattle to make production economically viable. But the clay surface used in many cattle pens can end up in manure, damaging biodigester machinery. Many feedlots are converting to roller compacted concrete, which improves cattle efficiency and eliminates the problem of clay in the biogas process. This, too, is costly.

The development of communal digesters could allow smaller farms to participate in the production of biogas. But support to help cover the upfront costs—and a streamlined process to obtain it—will be critical.

Key challenge: 93 MT overall

Without change: 137 MT

Game changers: Advanced ag-tech that cuts emissions, enables more carbon to be stored in soil and leads to more production on less land

The potential: To enable 54 MT in potential emissions reductions (or as much as 76 MT when soil sequestration is added)

Canada has a long history of agricultural innovation. The development of Marquis Wheat in 1904 was vital to the boom in Prairie crop yields that followed. Canola, created in Saskatchewan in the 1960s, is now one of the world’s most important oilseed crops. The grain auger was invented in Canada. And air seeders bearing the logo of Saskatchewan’s Seed Hawk can now be found on fields from Australia to Europe.

All of these developments fueled step changes in the productivity of Canadian agriculture. The next generation of technologies will need to do more than that. Indeed, all of the emissions reductions envisioned in this paper will in some way rely on technology—innovations like CCUS, biodigesters and precision tools. Technology will also be critical to producing more food on less land and by extension, avoiding the conversion of land into cropland. Our estimates suggest we can avoid 20MT of emissions by preventing land use change between now and 2050. Storing more carbon in soil—producing negative emissions—will also depend on increasingly sophisticated devices like soil sensors and drones that enable the market innovation necessary to accelerate new approaches like regenerative agriculture.

Canada’s heft in global agriculture markets, its longstanding expertise in crop science and its newfound strength in artificial intelligence and data science, position us well to lead in some areas of this race. Yet when it comes to drawing private investment to homegrown innovation, we’re falling behind. Of roughly US$36 billion in global venture capital and private equity investments in ag-tech since 2017, Canada received just 3%, or US$1 billion. The U.S. captured US$20 billion or 55% of investments.

Critically, private equity and venture capital investment has lagged in some of the areas that have historically reaped the largest rewards for Canadian agriculture. As we look to lower emissions, crop genetics and soil science (including microbiome research) hold some of the greatest potential for boosting production on existing farmland, cutting carbon emissions and improving resilience to droughts and flooding. While much of our research has been focused “above the soil” in the past, scientists are increasingly turning their attention to the potential of root structures and soil microbiomes to cut emissions. But so far, private investment in these fields hasn’t rushed to Canada. Of total global private equity and venture capital investment of roughly US$10 billion since 2017, our ventures in crop genetics have drawn only US$82 million.

In addition, much of the investment Canada is attracting isn’t going to the kinds of technologies we need now to transition to a more sustainable agriculture and food sector. Globally, over half of private investment in ag-tech in 2021 was in sustainable practices. But in Canada, most investments are focused on digitization and automation, technology designed with productivity, not sustainability, in mind.

As we work to deploy these solutions today we’ll also need to keep an eye to the future, investing in earlier stage technologies that can help us adapt our food systems to climate change. “Controlled environment” agriculture, such as greenhouses and vertical farms that allow crops to be grown indoors and in stacked layers, is taking off around the world. Canada currently imports fresh produce at a low cost from regions that are far more vulnerable to climate change. Tech-based alternatives like these could help us maintain domestic food security in an increasingly volatile world of climate and political disruptions. Meantime, cellular agriculture and precision fermentation technologies, which are advancing rapidly, could increasingly provide consumers with alternatives to meat and dairy products.

“I think plant breeding could really do it for us. If you look at all the advances we’ve made in higher yields, disease, resistance, all these kinds of traits and that’s all been focused above ground. There’s an equal opportunity below ground to make all kinds of significant advancements.”

Stuart Smyth, Associate Professor, College of Agriculture and Bioresources, University of Saskatchewan

The challenges: Artificial intelligence and data science, engineering, the “Internet of Things”, including sensors and drones, as well as biotechnology, are critical to the development of modern ag-tech. So are the skills that go with them. Yet efforts to draw this specialized talent and develop these skills among youth have fallen short of our needs.

Most support for Canadian research comes from public funding—which has been behind many of our successes. Marquis Wheat, which dramatically improved yields in the Prairies in the early 1900s, was developed through Dominion Experimental Farms—a system of stations, operated by the federal government, which investigated agricultural problems and created new techniques to assist farmers. Current funding programs can be onerous for researchers, particularly for emerging technologies that don’t fall easily into specific funding categories. And certain regulatory requirements—including those surrounding novel plant traits—can act as barriers to approval and investment in emerging areas of plant science like gene editing.

While Canadian researchers continue to rely on public investment, other countries including the U.S., are seeing most of their overall research dollars come from the private sector. Competing in the next era of agriculture will depend on our ability to mobilize more of this capital.

Fighting food waste

Though a lot of waste happens during production and processing, just 14% of that is avoidable. Technological advancements have done much to eliminate food loss at the production stage, an effort driven in part by the cost savings it generates.

Among consumers, the problem of food waste is far more entrenched. Studies suggest 18% of all food produced is wasted in ways that could be avoided. Almost half of that avoidable waste comes from hotels, restaurants and households, with consumers in wealthier countries far more likely to waste food than those in poorer countries. As that food decomposes in landfills, it releases greenhouse gases, as much as 12 MT—when measured from end-to-end.

Solving the problem of consumer food waste means tackling a cluster of causes. These include time scarcity (consumers lack the time they need to plan meals and use food before it goes bad); a lack of education on how to prevent food waste through more thoughtful storage and use of cooking waste like vegetable stalks; and retail promotions that encourage consumers to buy more than they need.

In addition to cutting food loss, industry has done much to extend the shelf life of food through packaging and other controls. More novel packaging solutions are underway that use plant-based and microbial packaging and coating solutions to do the same. Sensors can tell us when food has actually spoiled rather than leaving consumers to rely on best before dates. And new business models are emerging, such as those that transform food that doesn’t meet retail standards into poultry feed and other uses.

But ultimately, solving the problem of food waste will depend on us.

Recommendations: Seeding change

Cutting our greenhouse gas emissions, while also meeting our responsibility to feed the world, is a challenge rife with uncertainty. With many agricultural technologies and farm practices still in nascent stages, and widespread adoption still elusive, questions will continue to hang over our actions.

This risks paralyzing our efforts at a time when there isn’t time to lose. The stakes of the current food crisis are staggering: shortages and high prices for staple goods, have put the lives and livelihoods of 345 million people in immediate danger of acute food insecurity.24 Low income countries, many of which depend on imports from Ukraine and Russia, including Somalia, South Sudan and Yemen, are among the most vulnerable. In North America and other higher income countries, soaring food prices due to shortages and post-pandemic inflation are also dominating public agendas.

The urgency of the situation means we’ll need to act boldly using the best tools we have today. And we’ll need to do it together. Policymakers, private businesses and producers will need to collaborate in new ways as we pursue a national strategy designed to support farmers. This begins by focusing on the building blocks we’ve identified above, and on the key pillars of technology, people, policy, and economics. Working with BCG Centre for Canada’s Future and the Arrell Food Institute, we’ll explore each of these pillars in depth in the coming months.

Building an agricultural sector fit for an age of climate disruption is a challenge unlike any we’ve faced. But few countries are better positioned than Canada to confront it.

The global threat of food insecurity growing. So, too, is our ability to lead a new age of innovation to both harvest our land and sustain it.

Planting a paradigm shift: Building the 4 key pillars of a low emissions food strategy

Policy

Establish a national plan for a low-emissions agriculture sector. Our plan for cutting emissions must take all stakeholders into account and rally not just farmers, but investors, private business and Canadians. Producing food more sustainably will mean making tough choices and supporting investment in key technologies, like carbon capture, utilization and storage (CCUS). It will also mean doing a better job of marketing Canada’s sustainable food to the world.

Lead efforts to create global alignment on a low-emissions food standard. Roughly 61% of our agricultural emissions are tied to goods that are ultimately exported. Advancing an emissions reduction strategy that’s misaligned with our key export markets could create friction in our trading relationships. We need to align trading partners around a common set of goals, indicators and GHG measurement, reporting and verification protocols. Canada, a longstanding supporter of free trade, and a global leader in multilateral processes, can lead these efforts.

Integrate agricultural strategies with energy strategies. Farmers are increasingly embracing opportunities to generate renewable natural gas from their operations. Integrating these efforts with a national energy strategy could help accelerate the deployment of clean energy both on and off the farm.

Technology

Create a central funding body for research and development, operating in close partnership with academia and the private sector. Many of the most promising and advanced areas of Canadian agricultural research don’t fit within current funding categories. A more centralized system such as in the United States Department of Agriculture, could develop a more holistic, nationwide view of where support and innovation is needed. The leadership shown by federal governments in creating the innovation super clusters provides a playbook for how Canada can super charge agri-food research and innovation.

Focus on technologies that hold the most promise to cut emissions. As we target funding to technology that accelerates productivity, we need to also attract more investment to technologies that cut emissions from key drivers in the supply chain—innovations like anaerobic digesters, feed additives and CCUS. Funding should also be focused on those technologies that enable sustainable practices to be adopted and rewarded, like soil sensors, and precision technologies.

Create innovative tax and financial incentives to spur more private investment. Accelerating private investment in Canadian agtech will mean thinking more creatively about the tax and financial incentives we have in place. We need to encourage the automation that will be key to our agricultural productivity and international competitiveness—and that will draw more capital to the technologies that will drive the future of low emissions farming. Expanding accelerated depreciation beyond tangible assets to include artificial intelligence and other agtechs is one possibility.

Economics

Make it pay. Forcing farmers to pay for emissions they already produce could add pressure to high food prices. A better approach is to compensate farmers for reducing them. Yet existing models like carbon credits are insufficient and place an unequal burden on the farmer. A national standard for measuring the impact of emissions-cutting activities, including a mechanism for measuring, reporting and verifying (MRV) carbon stored in soils, could be critical to compensating farmers and to empowering policymakers and financial institutions to mobilize support. This standard—also key to attracting investment—will need to be designed and regulated on a national basis and aligned internationally with our major trading partners.

Share the risk. For farmers, the adopting of emissions-cutting technology adds more uncertainty to a business already weighted with risk. Governments and other companies in the agricultural value chain have an important role to play in sharing the risk burden. That’ll mean insuring against yield losses for farmers who adopt sustainable practices. For example, right now there is no incentive for sustainable agriculture under crop insurance schemes though these practices are proven to reduce the impact of flooding and drought. Crop insurers should be willing to adjust premiums to reflect these shifting risks.

People

Build the skills. Leverage the Labour Market Information Council to pinpoint the skills farmers need to shift toward a more resilient food system. As we’ve noted in previous research, digital skills will be critical to the future of food production.25 So too will knowing how to apply tools in ways that cut emissions. Beyond data and technology, some farmers will need support to employ regenerative agriculture techniques and other tools on the farm. Experiential learning platforms including hands-on mentorship and co-op programs can accelerate this transition.

Broaden the talent pool. The lack of awareness about the potential for a fulfilling career in agriculture has hampered recruitment of individuals with the coding, artificial intelligence and data science skills critical to the future of food. Yet few sectors hold greater potential for innovation than agriculture. Educating students on the opportunities in the field—through co-ops, outreach and liaison programs—will be critical to bringing their talents to the challenge.

For more, go to rbc.com/climate.

Download the Report

\

Contributors:

RBC

Naomi Powell, Managing Editor, Economics and Thought Leadership

John Stackhouse, Senior Vice President

Colin Guldimann, Economist

Farah Huq, Senior Director, Content Strategy

Darren Chow, Senior Manager, Digital Media

Trinh Theresa Do, Senior Manager, Thought Leadership Strategy

Zeba Khan, Manager, Digital Publishing

Aidan Smith-Edgell, Research Associate

Kitty Wu, Intern

Gwen Paddock, Director, Sustainability & Climate – Agriculture

Ryan Riese, National Director, Agriculture

Boston Consulting Group

Keith Halliday, Director, Centre for Canada’s Future

Kilian Berz, Managing Director and Senior Partner

Shalini Unnikrishnan, Managing Director and Partner