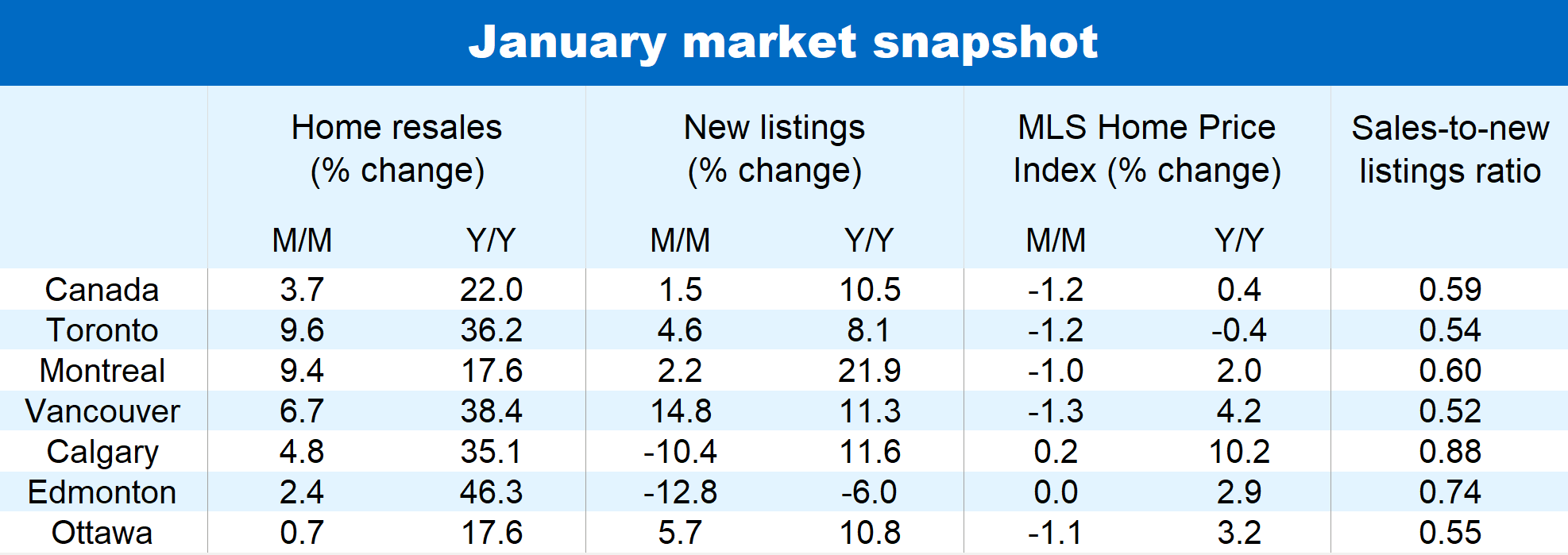

It may be the unusually mild weather or the modest drop in fixed mortgage rates since November—or both—but Canadian house hunters have more energy this winter. Importantly, they’re landing more deals. Home resales in Canada increased for the second month in a row in January, rising 3.7% from December. Resales are back up to where they were last summer including the December advance. It’s still historically soft though, given recent cyclical lows. The upturn suggests that the sharp correction triggered by soaring interest rates has likely run its course.

What it hasn’t done yet is turnaround declining prices. The MLS Home Price Index continues to drift lower, falling 1.2% month-over-month in January nationwide and declining 5% since August 2023. Most local markets recorded price drops between December and January including Vancouver, Winnipeg, Toronto, Hamilton, Ottawa, Montreal, Moncton and Halifax. The huge loss of affordability during the pandemic remains the dominant force weighing on property values. Calgary is among the few markets bucking the trend with exceptionally tight supply-demand conditions keeping prices on an upward trajectory.

However, the broader pricing picture could be approaching an inflection point. This winter’s renewed market vigour is making it a more competitive environment for buyers. They vie for a shrinking inventory of homes for sale—despite new listings rising modestly by 1.5% in January. We think a bottom could form around mid-year and forecast the national benchmark price to gradually appreciate in the second half of 2024.

Busier activity in most provinces

January was a busier month in most provinces. Ontario and British Columbia led way with strong sales gains in Toronto (9.6% m/m), Hamilton (12.6%), the Niagara region (18.5%), Vancouver (6.7%) and the Fraser Valley (15.9%). Other parts of the country also saw a noticeable pick up in activity including Montreal (9.4%) and Calgary (4.8%).

In the majority of cases, the rise in residential transactions is from historically low levels. The market can still generally be best described as slow. The main exceptions are Alberta (including Calgary and Edmonton) and Saskatchewan (including Regina and Saskatoon) where home resales are running some 20% to 80% above pre-pandemic levels.

A word of caution

The coming months will confirm whether the recent uptick marks the end of the housing market correction and the start of a recovery phase. Spotting trend shifts in December and January—seasonal low points—can be tricky because large adjustment factors are used when removing seasonal influences from the statistics. These factors can exaggerate month-to-month changes—up or down. Upcoming data, especially in the spring, will give a more reliable read of underlying trends.

Interest rates to dictate market outcome this year

We expect slow activity and softer prices to persist in the early part of the year as the Bank of Canada maintains its policy rate at a two-decade high and home ownership stays out of reach for many potential buyers. But, we think a pivot towards rate cuts mid-year will get the wheels turning faster over the second half—perhaps even sooner. There will be a lot of pent-up demand to satisfy once confidence returns, which could heat things up in a hurry. However, poor affordability conditions will restrain the recovery and make it a gradual liftoff. The larger window of opportunity for buyers is likely to open only after interest rates have dropped materially—something we foresee in late 2024 or into 2025. That’s especially the case for first-time buyers who may be more financially constrained. See our housing market outlook report for more on our forecast.

See PDF with complete charts

Robert Hogue is an Assistant Chief Economist at RBC responsible for providing analysis and forecasts on the Canadian housing market and provincial economies. He joined RBC in 2008.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.